Appears like fintech is working its magic.

Based mostly on an inquiry from a reporter, my colleagues JP Aubry, Yimeng Yin, and Angie Chen have been playing around with information on holdings of Roth IRAs from the Federal Reserve’s 2022 Survey of Consumer Finances.

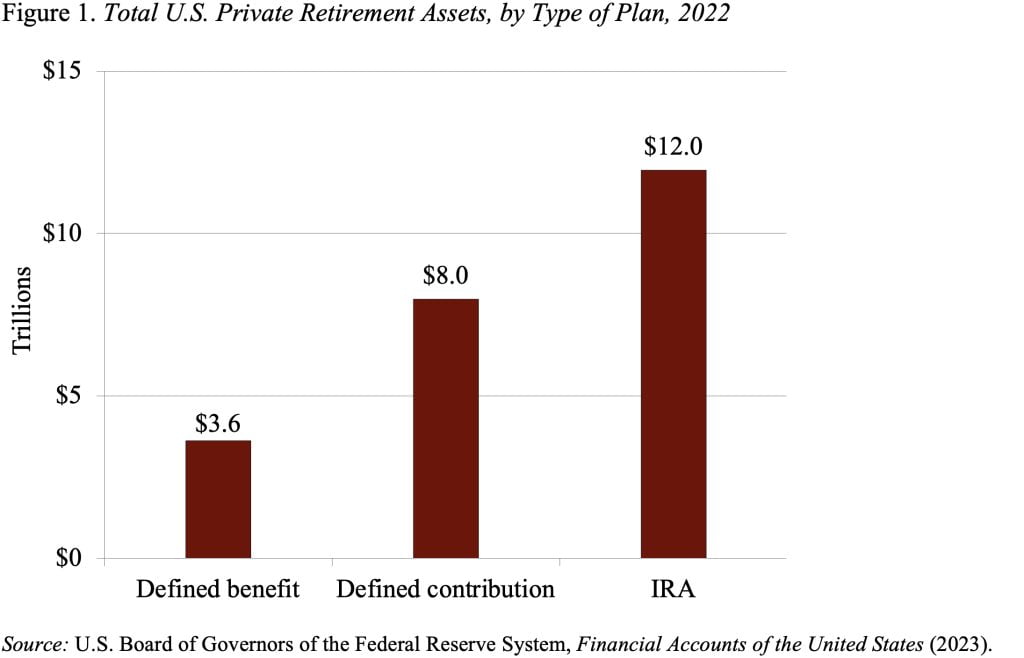

Since belongings in IRAs account for greater than half of all belongings in personal sector retirement plans – far exceeding these in both outlined profit or outlined contribution (DC) plans – something occurring on this house is vital (see Determine 1).

Furthermore, Roth IRAs are the automobile used within the Auto-IRA applications, which have now unfold to 14 states. These applications require employers with out a plan to routinely enroll their employees in a Roth IRA – the employee can choose out. So, are these state initiatives the supply of the expansion or does it come from fintech companies equivalent to Robinhood, which have made it very simple to purchase and promote monetary belongings and to contribute to retirement accounts?

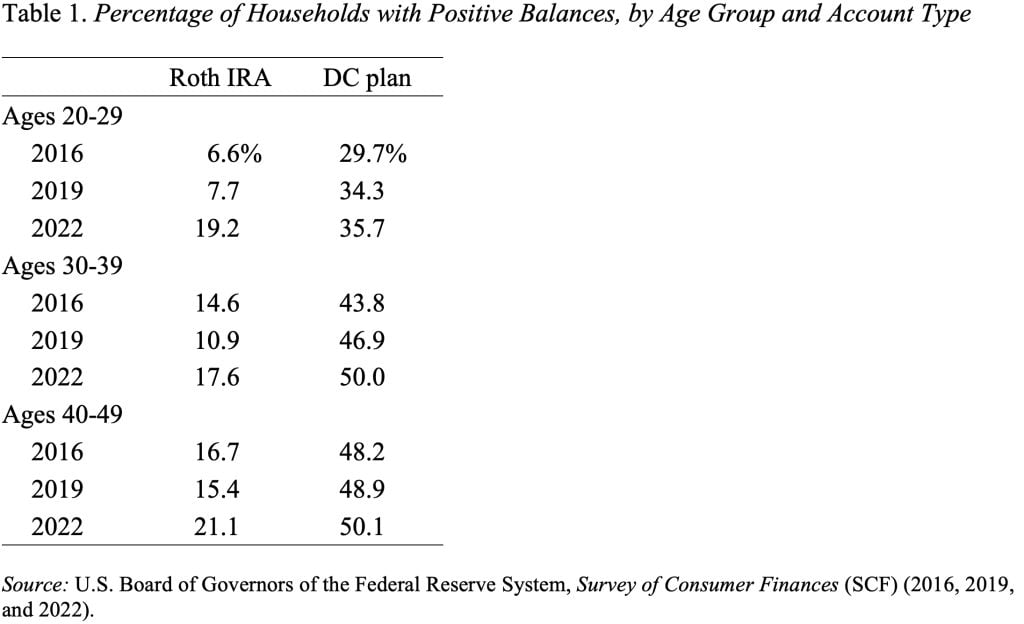

The journey began with JP and Yimeng figuring out that the share of younger households with a Roth IRA has elevated quite a bit since 2016 (see Desk 1). Amongst households with the top ages 20-29, the share has tripled from 6.6 p.c in 2016 to 19.2 p.c in 2022. Nothing related appears to be occurring for older age teams or by way of DC plan participation.

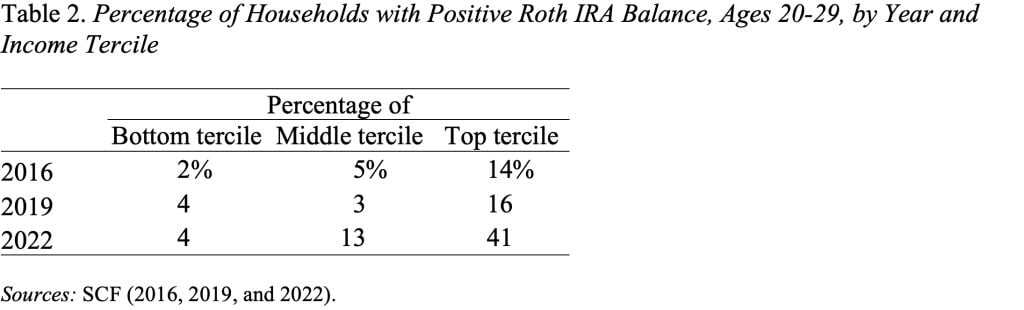

Who’re these folks opening Roth IRAs? Angie did some cross tabs by earnings tercile, which you’ll see in Desk 2. The rise in Roths is concentrated among the many prime tercile – the third of households with the best incomes. The center tercile additionally reveals a rise – albeit from actually low ranges. It’s trying much more like a fintech phenomenon than the affect of the state Auto-IRA initiatives, that are typically targeted on lower-paid employees.

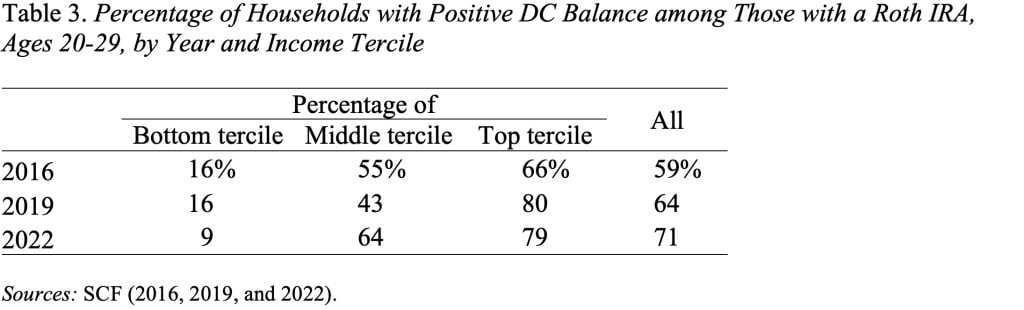

The query nonetheless stays whether or not the expansion in Roths displays a rise in protection or simply households already lined including one other account. Desk 3 reveals that for the highest tercile – the place with all of the motion – 80 p.c of the households with a Roth IRA already had optimistic balances in a DC plan.

The underside line appears to be that if know-how makes it very easy to save lots of in tax-advantaged accounts, the tech-savvy with cash will reap the benefits of the chance.

{kind=link}