The temporary’s key findings are:

- Writing a will ensures an individual’s wealth goes to meant recipients, stopping main property like a home from being break up up amongst many heirs.

- But many individuals don’t have a will, notably lower-income and non-White households.

- Utilizing a survey experiment, the evaluation explores whether or not buyer interactions with banks might encourage will-writing.

- The outcomes present that:

- combining will-writing with taking out a mortgage – a posh and traumatic occasion – is a nasty concept;

- providing individuals cash helps, however primarily those that want it the least; and

- linking will-writing to a less complicated activity, like opening an account, is a way more efficient choice, particularly for deprived teams.

Introduction

Writing a will can enhance the transmission of wealth throughout generations by stopping the dissipation of property – akin to a household dwelling divided amongst a number of heirs – and by encouraging donors to save lots of for his or her beneficiaries. Regardless of the benefits of having a will, the proportion of households with a will is surprisingly low. For these ages 50+, lower than half of family heads have a will. By age 70, that share will increase to 67 %, however the shares are a lot decrease for much less rich households and for Black and Hispanic households. The query is whether or not focused bequests will be elevated via an intervention that promotes will-writing.

To reply that query, this temporary, which relies on a latest examine, studies on the outcomes of an internet survey and experiment administered by NORC on the College of Chicago. The members are requested a sequence of questions on whether or not or not they’ve a will and why. These and not using a will then take part in an experiment the place they’re randomly assigned to considered one of 4 therapy teams to find out whether or not numerous incentives would encourage them to jot down a will.

The dialogue proceeds as follows. The primary part offers some background on the significance of wills and can standing by race/ethnicity. The second part describes the survey. The third part presents the outcomes relating to who has and doesn’t have a will and why. The fourth part presents the outcomes of the experiment, which present that setting issues – combining writing a will with taking out a mortgage is a nasty concept; providing individuals cash helps; and financial incentives are simpler for many who are extra financially refined and for White respondents. The ultimate part concludes that most individuals and not using a will intend to jot down one sooner or later and that incentives can have an effect on this final result. Nevertheless, including a will to an already traumatic occasion akin to taking out a mortgage has a unfavorable impact on intentions.

The Significance of Wills

The distinction between having some wealth and relying solely on present revenue is large. Wealth offers a buffer that permits households to face up to emergencies or to cowl expenditures within the face of unemployment. It permits individuals to take dangers when deciding on jobs – forgoing some compensation up entrance for extra revenue later. It offers households with the sources for a down cost on a home in an space with good faculties, thereby enhancing the prospects for his or her households. For low-and middle-income youngsters, one of many most important methods to amass some wealth is thru an inheritance. Mother and father can go away their dwelling or modest monetary property to their youngsters, who in flip usually tend to go away a bequest to their youngsters. These bequests could also be small, however they are often life-changing.

The simplest manner to make sure that wealth transfers go to the meant recipients is for the donor to have a will. And not using a will, property can get dispersed amongst a number of heirs, which generally is a explicit downside for individuals whose main asset is their dwelling. On this case, all of the heirs should coordinate earlier than sustaining or promoting the property. When it comes to concentrating on bequests to the specified beneficiaries, states have established default guidelines, which might obtain an affordable final result for a lot of conventional households, however can produce the fallacious final result when the meant beneficiaries are usually not associated by blood, marriage, or adoption or when property are exhausting to divide (like a home, moderately than monetary property).

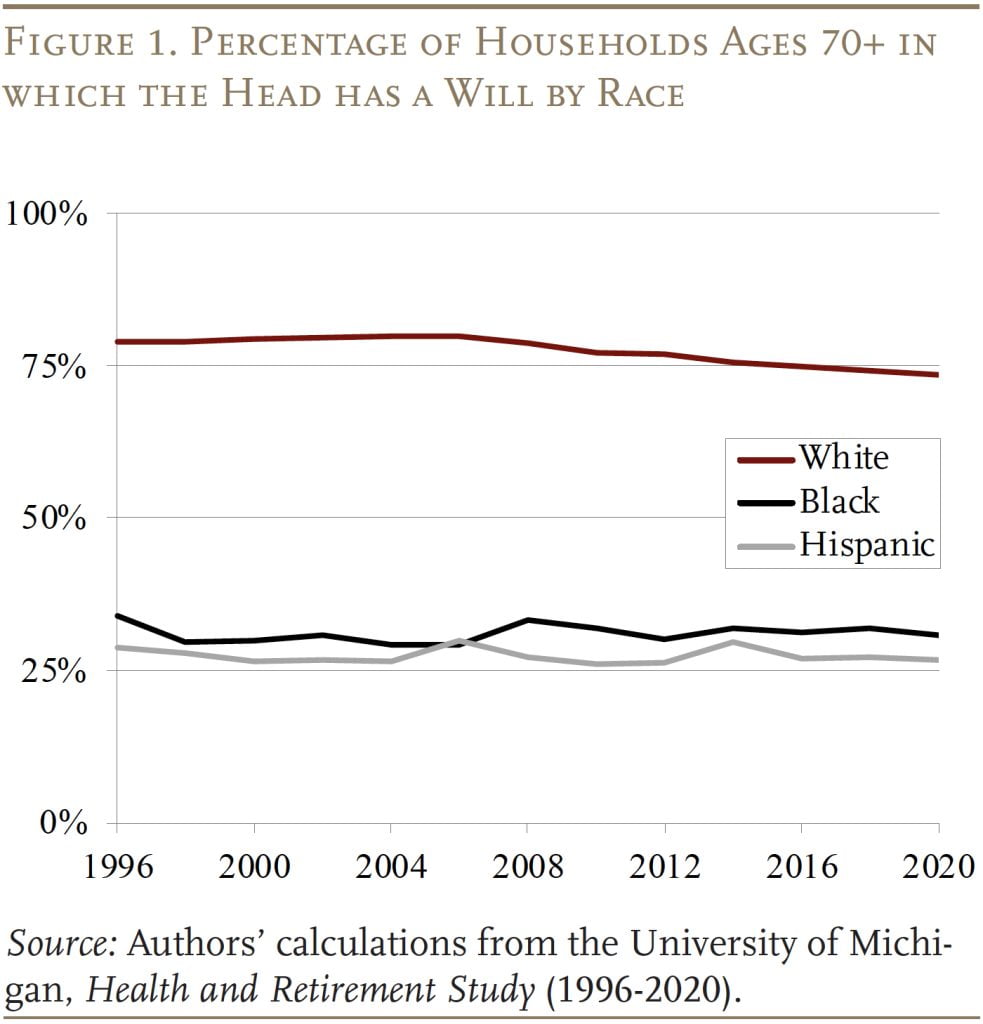

Regardless of the benefits of having a will solely about two-thirds of households with heads ages 70 and older had a will in 2020, and the share of White households with a will was greater than twice that for Black and Hispanic households (see Determine 1). Our earlier examine on wills additionally confirmed {that a} vital distinction persists even after controlling for different demographic traits, well being, wealth, schooling, and marital standing. One cause for this distinction is that individuals who obtain an inheritance usually tend to go away a bequest, and Black, Hispanic, and different non-White respondents are considerably much less prone to report ever having obtained an inheritance than Whites, even after controlling for different demographics and schooling.

Briefly, many households can be higher off if they’d a will to switch their property to their focused survivors, and a survey is required to see whether or not interventions are potential to encourage extra will-writing.

The Survey

The survey was performed utilizing the AmeriSpeak panel run by NORC on the College of Chicago. The panel is nationally consultant, and members have been eligible for this examine in the event that they have been ages 25 and older. The five-minute survey was performed on-line in April 2023 and included 3,047 respondents. The panel incorporates demographic particulars, akin to gender, race, schooling, and marital standing. To complement this baseline data, the survey additionally included questions on whether or not the respondent had youngsters.

Subsequent, the survey requested in regards to the particular person’s “will” standing. Does the person have a will? If sure, then at what age did they set up a will? What motivated them to jot down a will? What’s the possible measurement of their property? To whom will these property be bequeathed? If the person doesn’t have a will, then why not? How a lot does the person have in whole property? Does the person intend to jot down a will?

The survey then turned to an experiment to check the effectiveness of various therapies to extend will-writing for these and not using a will. Respondents have been randomly assigned to considered one of 4 teams. After every choice, members within the therapy teams have been requested whether or not they would seize the chance to jot down a will.

Management Group: Do you plan to jot down a will?

Therapy Group 1: If the financial institution provided the chance to determine a will (with free authorized and monetary recommendation) on the time of signing for the mortgage, would you’re taking up that provide?

Therapy Group 2: If the financial institution provided the chance to determine a will (with free authorized and monetary recommendation) on the time of signing for the mortgage and gave you a $500 incentive to take action, would you’re taking up that provide?

Therapy Group 3: Think about you might be opening a checking, financial savings, or funding account at a financial institution. If the financial institution provided the chance to determine a will (with free authorized and monetary recommendation) whenever you opened the account, would you’re taking up that provide?

The subsequent part studies on the need standing and causes for that standing, after which the next part summarizes the outcomes of the experiment.

Outcomes from the Base Survey

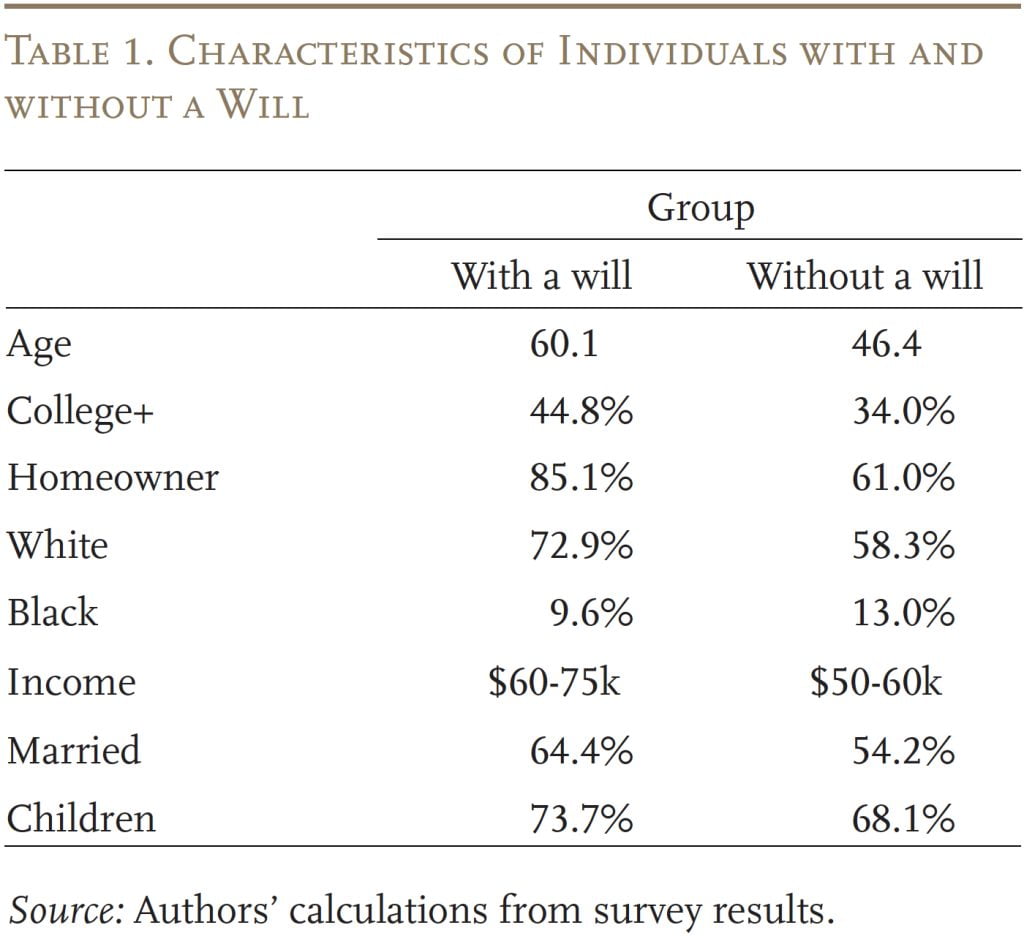

The survey confirmed that 34 % of respondents had a will. These people have been older, with extra schooling, extra prone to personal a house, extra prone to be White, and had considerably greater revenue (see Desk 1).

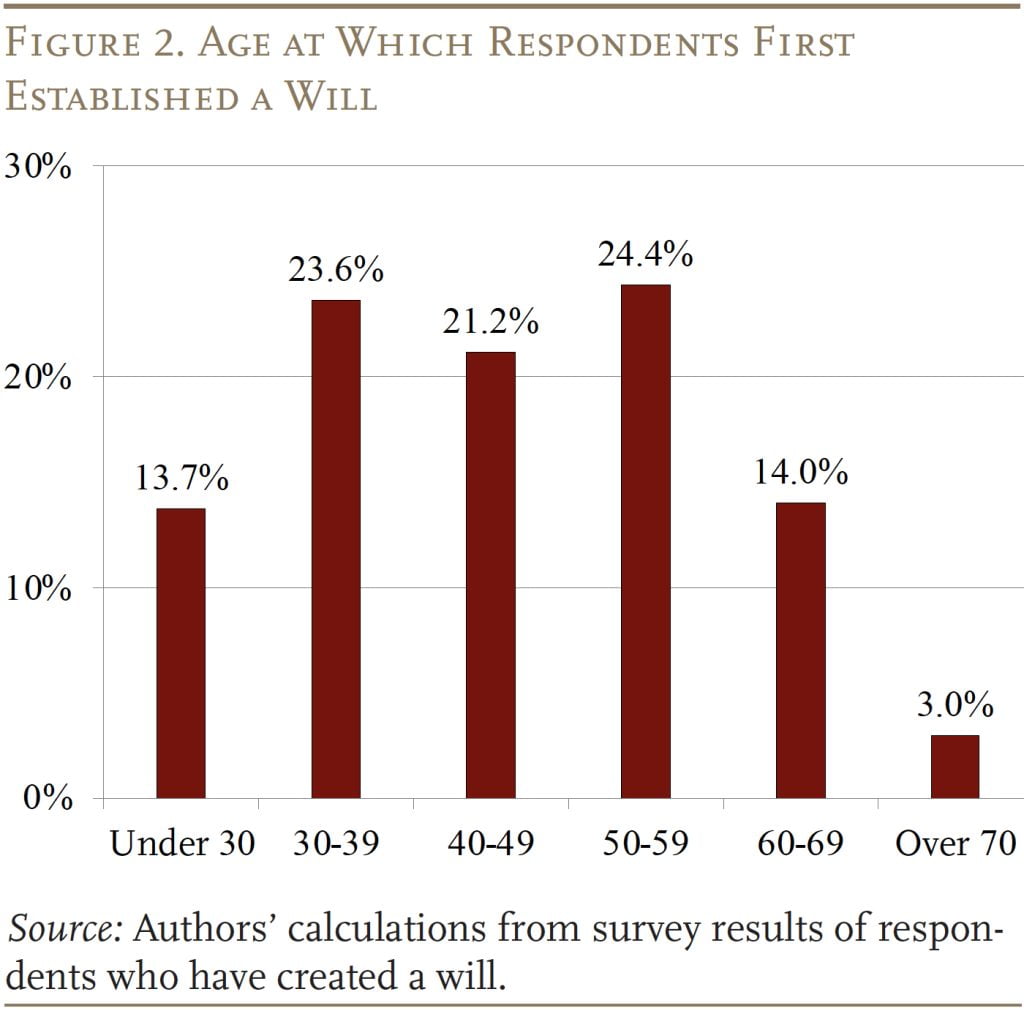

Most people arrange their wills of their 30s, 40s, or 50s (see Determine 2).

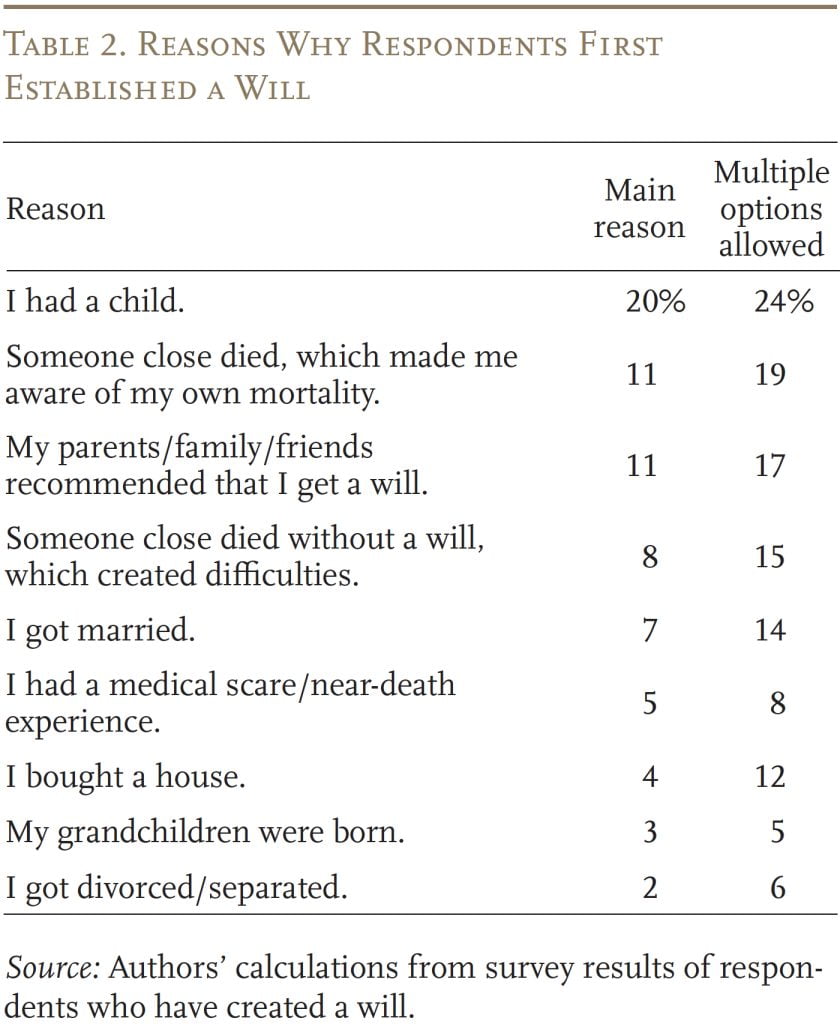

An important motivating life occasion for writing a will was having a toddler (see Desk 2). The subsequent two causes have been extra exterior: 1) somebody near the person died, highlighting their very own mortality; and a pair of) mother and father/household/good friend really helpful the person set up a will.

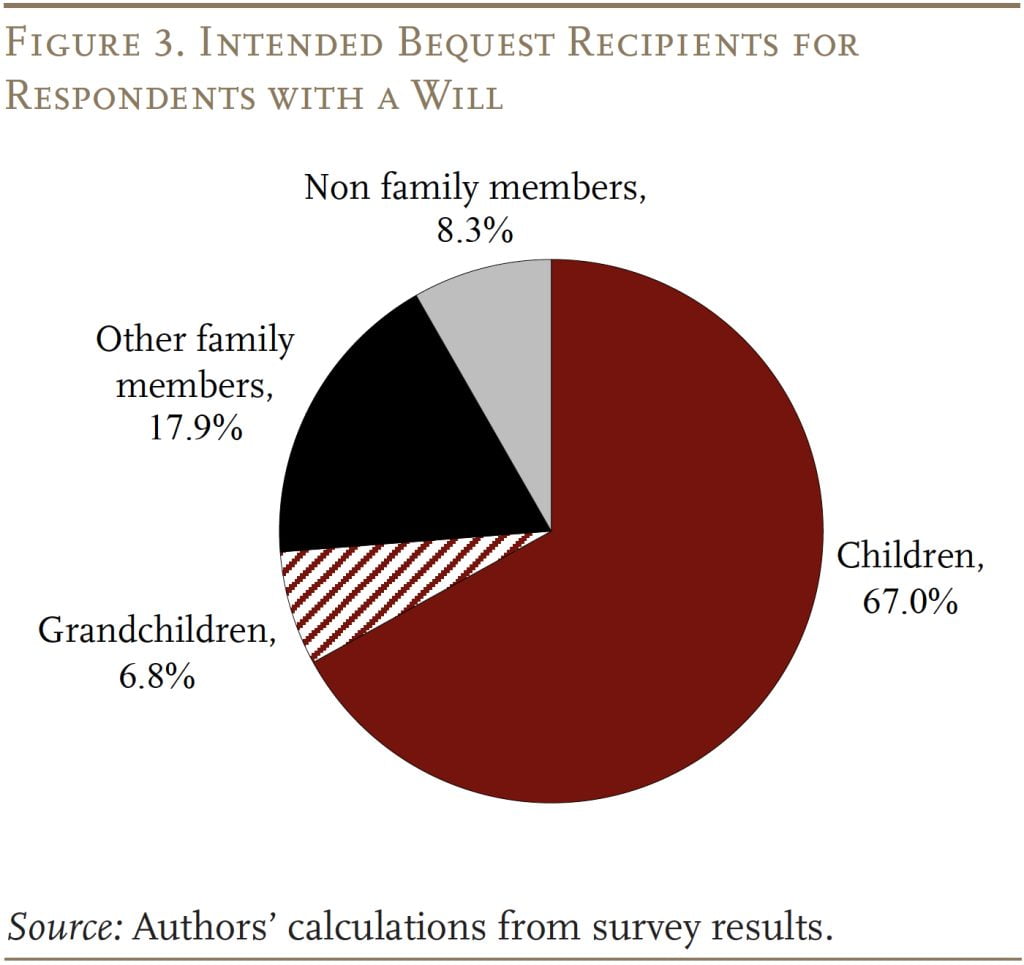

The survey additionally asks about meant recipients of a will. The outcomes present that youngsters account for two-thirds of the whole and grandchildren 7 %. Different relations account for 18 % and non-family – each unrelated people and non secular or charitable organizations – 8 % (see Determine 3).

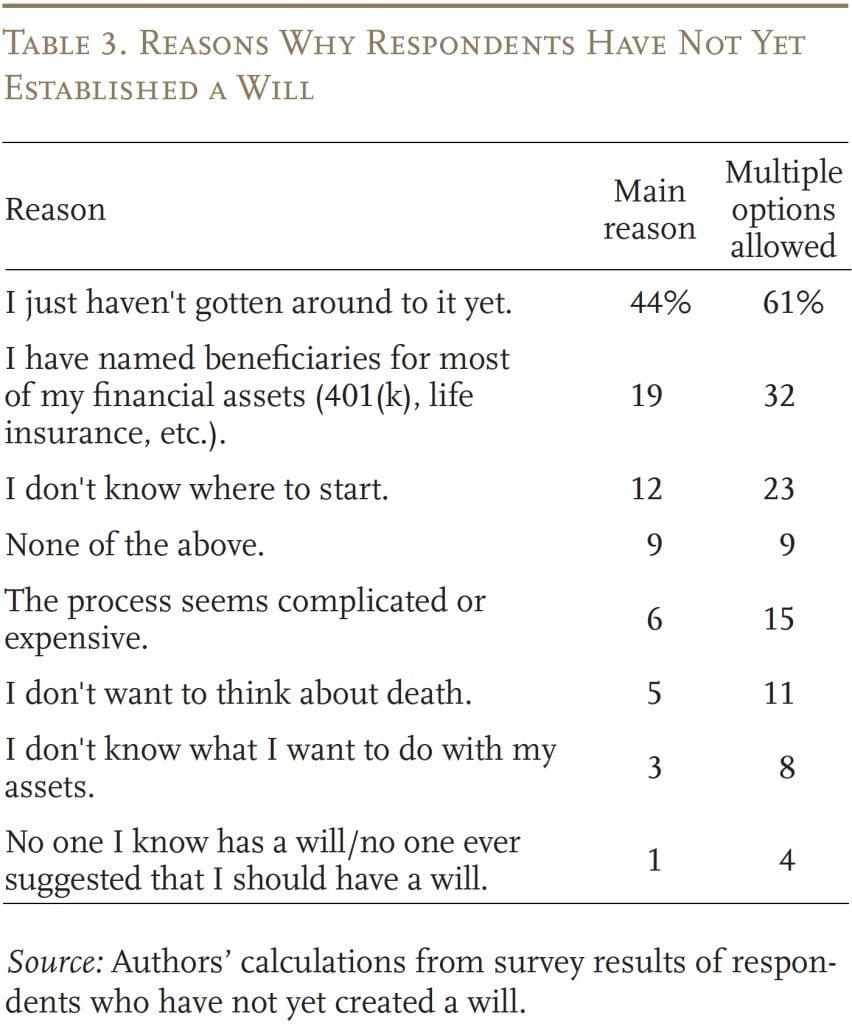

The remaining 66 % of individuals didn’t have a will. The foremost cause provided for not having a will was: “I simply haven’t bought round to it but,” (see Desk 3). This response is in step with earlier research exhibiting procrastination is a serious downside in terms of will-writing. The second main cause is that some could have thought they’d taken care of bequests, responding: “I’ve named beneficiaries for many of my monetary property (401(ok), life insurance coverage, and so on.)” Most of the different responses recommended that folks have been usually baffled by the method.

Outcomes from the Experiment

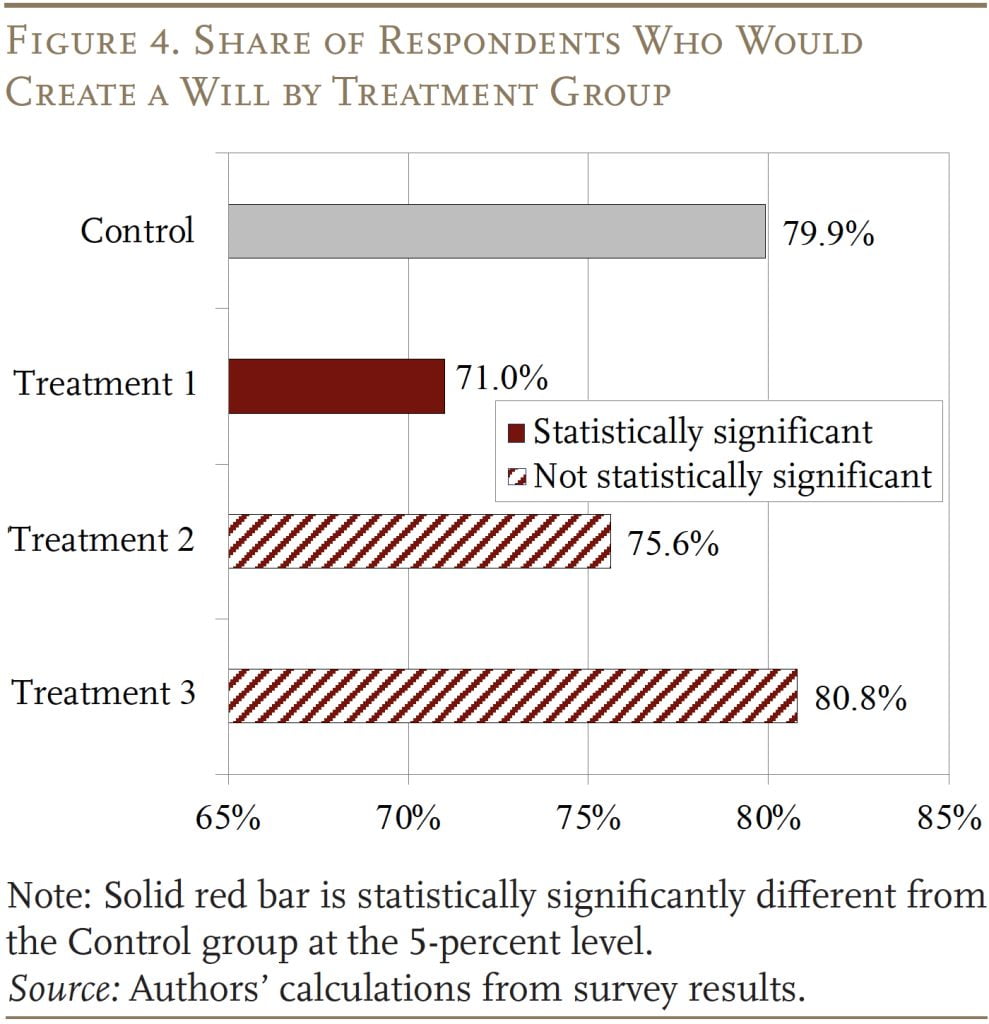

When it comes to the impression of the experimental therapy on the intention to jot down wills, the outcomes have been surprising – and at first disappointing – however, on reflection, do present some actual data. The disappointing information is that the primary two therapies, which related will-writing with the taking out of a mortgage, truly decreased the proportion of respondents who stated they meant to jot down a will (albeit solely statistically considerably for Therapy 1, see Determine 4). With none therapy, 79.9 % reported they meant to jot down a will; as soon as the query was linked to the mortgage course of, the proportion dropped to 71.0 % – even with the provide of “free authorized and monetary recommendation.” Including $500 to the proposal solely introduced the proportion midway again to the no-treatment degree. When the state of affairs modified from a mortgage atmosphere to easily opening a checking account, the proportion intending to jot down a will elevated to 80.8 %.

One situation with the above outcomes is that the one statistically vital coefficient is related to Therapy 1, which hyperlinks writing a will with taking out a mortgage. Neither Therapy 2 – providing $500 – nor Therapy 3 – offering a extra pleasing financial institution interplay akin to opening an account – produce statistically vital impacts. One potential clarification could also be that the Management group is just not fairly in step with the therapies in that it doesn’t have a time aspect. Contributors within the Management group are simply requested in the event that they intend to jot down a will, with no particular time-frame. In distinction, all three therapy teams are requested: “Would you’re taking up that provide?” That’s, they’re requested whether or not they would act at that second.

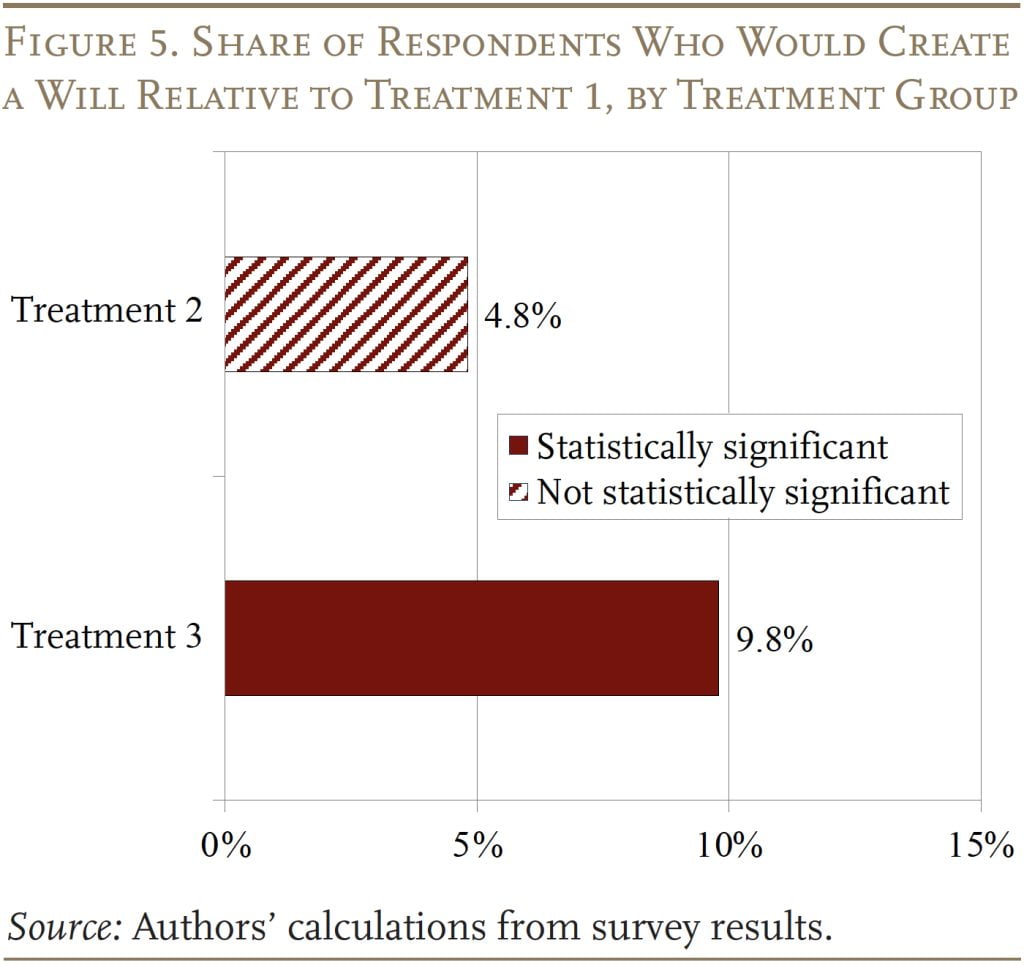

One solution to circumvent the timing inconsistency to realize extra details about the relative attraction of the three choices is to drop the Management group and easily evaluate the therapy teams amongst themselves. The outcomes of this train are proven in Determine 5. Right here, providing $500 has barely any impact, however – even with out the monetary incentive – merely altering the bottom occasion from taking out a mortgage to opening an account – Therapy 3 – will increase the share intending to jot down a will by 9.8 proportion factors.

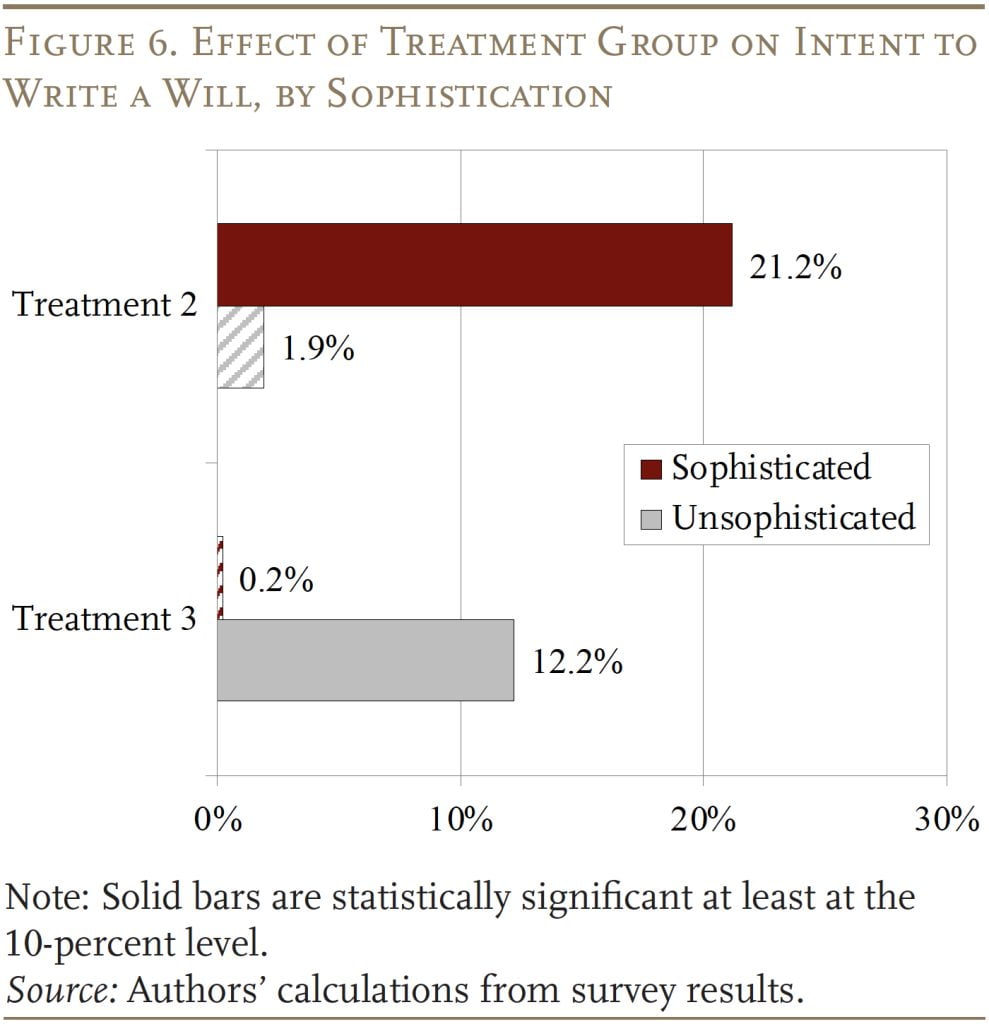

This formulation of the experiment will also be used to match the impression of the therapies by particular person traits. The primary train makes an attempt to separate the respondents by their sophistication, based mostly on their responses to questions on why they don’t have a will. This course of, which is extra artwork than science, included as “refined” those that reported that their major cause for not having a will was that they’d named beneficiaries for many of their monetary property. The unsophisticated have been those that provided any of the opposite responses.

The outcomes by sophistication, in Determine 6, present that providing a $500 cost for writing a will (Therapy 2) will increase the share intending to jot down a will by an enormous 21 proportion factors for the subtle, however by solely a statistically insignificant 1.9 proportion factors for the unsophisticated. In distinction, Therapy 3 (altering the setting) has a statistically vital impact on the unsophisticated – who’re possible overwhelmed by the mortgage course of – however not on the subtle.

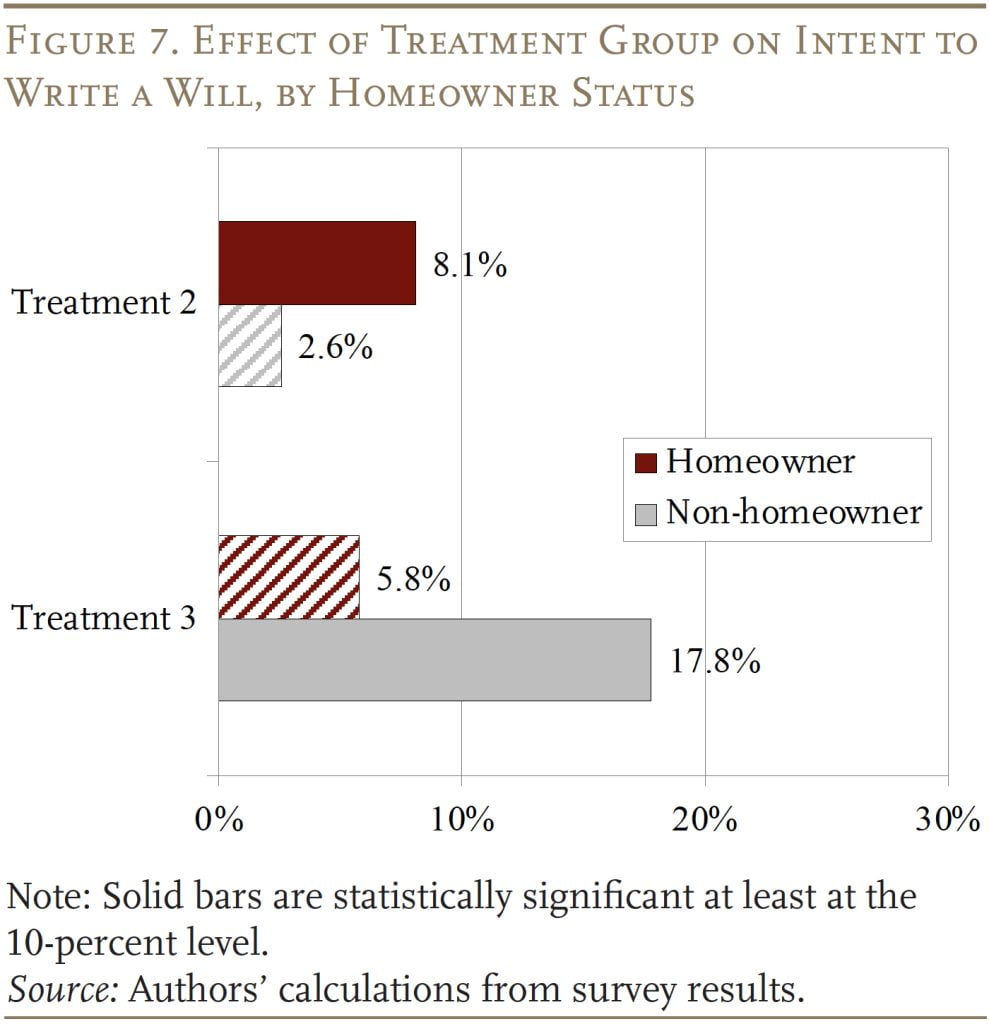

One other try and get at sophistication entails repeating the train for owners versus non-homeowners (see Determine 7). Including $500 to the provide (Therapy 2) has a slightly statistically vital impression relative to Therapy 1 for owners, however not for non-homeowners. In distinction, altering the setting (Therapy 3) incents extra will-writing for non-homeowners, whereas owners are a lot much less delicate to the setting. Householders may very well be much less intimidated by the mortgage course of due to prior expertise or as a result of a refinance mortgage is inherently much less onerous than an preliminary mortgage.

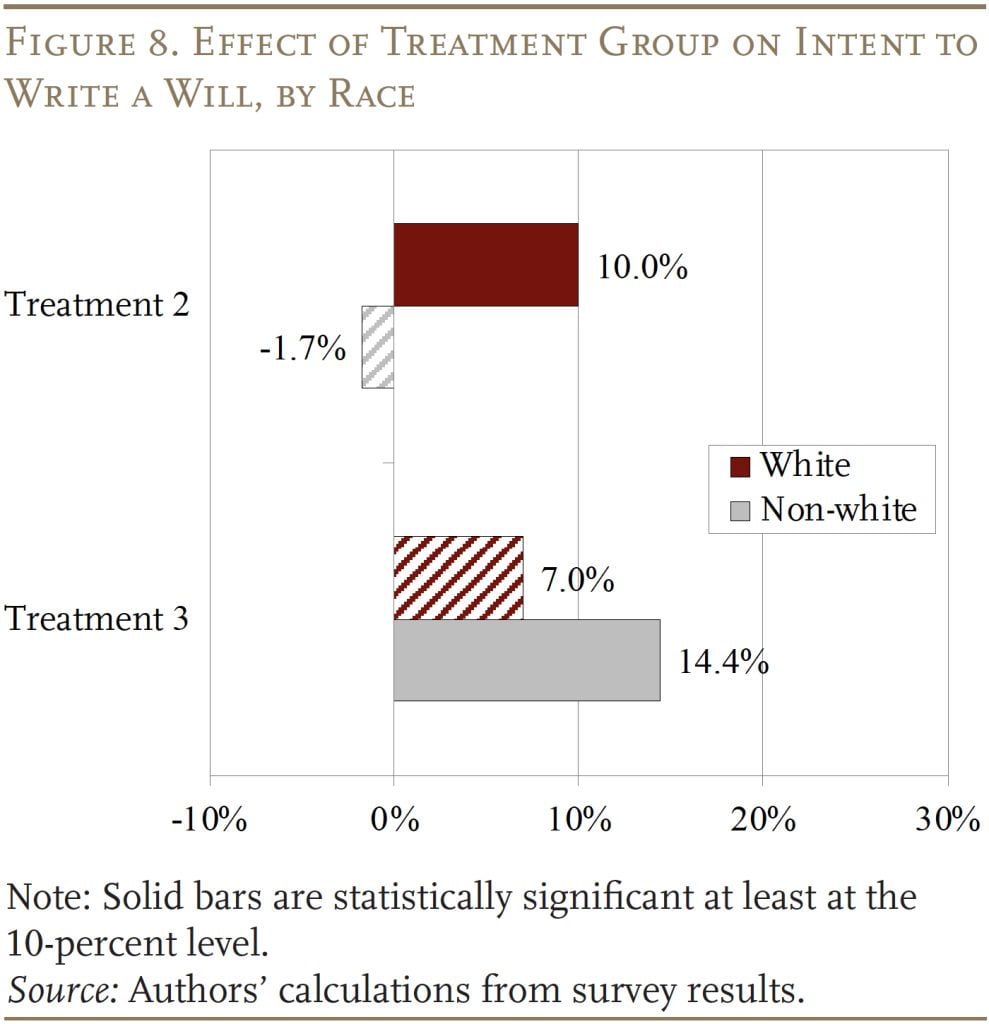

The ultimate groupings contain race and gender. The outcomes present that introducing the $500 incentive (Therapy 2) has a statistically vital impact on Whites, however non-White people don’t reply (see Determine 8). In distinction, Therapy 3 has a statistically vital impact just for Non-Whites, indicating that they seem to have a very robust desire for shifting the setting from taking out a mortgage to opening a checking account.

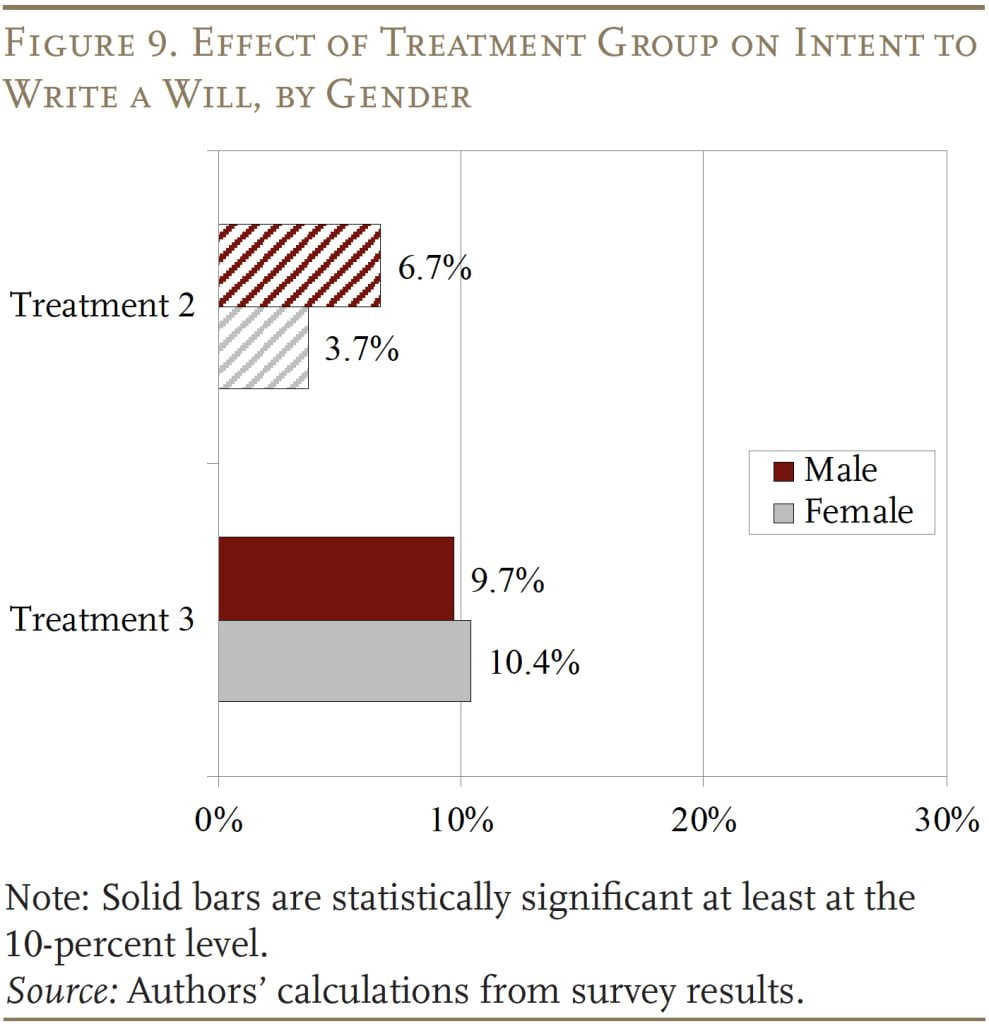

When it comes to gender, each genders seem equally impacted by Remedies 2 and three (see Determine 9). Neither are affected by the $500 monetary incentive, however each male and females can be extra inclined to jot down a will in a much less pressured setting.

The underside line from these outcomes is threefold. Most significantly, the setting issues. Attempting to mix a considerably sophisticated and emotional activity akin to writing a will with a sophisticated and exhausting course of like taking out a mortgage doesn’t work. Initially, it appeared like a good suggestion for the reason that mortgage occasion concerned specializing in many individuals’s largest asset – their dwelling – and peripherally on their different funds. One would possibly suppose that folks caring for a mortgage and a will on the identical time may gain advantage from economies of scale in assessing their monetary standing. However any economies look like swamped by sheer exhaustion. This discovering is especially true for these individuals the therapy is most meant to assist: the much less financially refined, non-homeowners, and Black respondents.

Alternatively, linking the writing of a will to a much less taxing interplay with the financial institution, akin to opening an account, does enhance intentions. The second situation is cash. Cash – on this case, $500 – will increase the proportion of some people prepared to jot down a will. The impact, nonetheless, is just half that related to altering the timing from taking out a mortgage to opening an account total, and largely concentrated in these teams who don’t want far more assist in writing a will. So, getting the setting proper is vital. Lastly, the impression relies upon considerably on the traits of the people. Those that may very well be categorised as extra financially refined – both by their responses or as a result of they’re already owners – are inclined to react considerably otherwise to the choice therapies than the unsophisticated. The impression additionally varies by race; Whites react extra to the $500, and non-White people extra to a change in setting.

Conclusion

Wills are necessary, notably for lower-income and non-White households the place the home is the foremost asset. So, incentives to extend will-writing might assist scale back the racial wealth hole. Whereas the notion of including will-writing to the mortgage course of turned out to be a nasty concept, the survey and the experiment present a number of data on who writes wills and why, and so they additionally counsel that setting issues and the impact of incentives varies considerably by particular person traits.

References

Aubry, Jean-Pierre, Alicia H. Munnell, and Gal Wettstein. 2023a. “Can Incentives Increase the Writing of Wills? An Experiment.” Working Paper 2023-27. Chestnut Hill, MA: Heart for Retirement Analysis at Boston School.

Aubry, Jean-Pierre, Alicia H. Munnell, and Gal Wettstein. 2023b. “Wills, Wealth, and Race.” Working Paper 2023-10. Chestnut Hill, MA: Heart for Retirement Analysis at Boston School.

Modern Research Undertaking. 1978. “A Comparison of Iowans’ Dispositive Preferences with Selected Provisions of the Iowa and Uniform Probate Codes.” Iowa Legislation Assessment 63: 1041-1070.

Fellows, M. L., R. J. Simon, and W. Rau. 1978. “Public Attitudes About Distribution at Death and Intestate Succession Laws in the United States.” American Bar Basis Analysis Journal 3(2): 319-391.

College of Michigan. Health and Retirement Study, 1996-2020. Ann Arbor, MI.

{kind=link}