This text is a part of a collection; click here to read Part 1.

Utilizing the portfolio return and volatility assumptions decided in Exhibit 1.1, we then reverse engineer fastened return assumptions and sustainable spending ranges for a desired retirement time horizon and focused chance of success. The funding portfolio is modeled utilizing 100,000 Monte Carlo simulations for these portfolio returns, assuming a lognormal distribution.

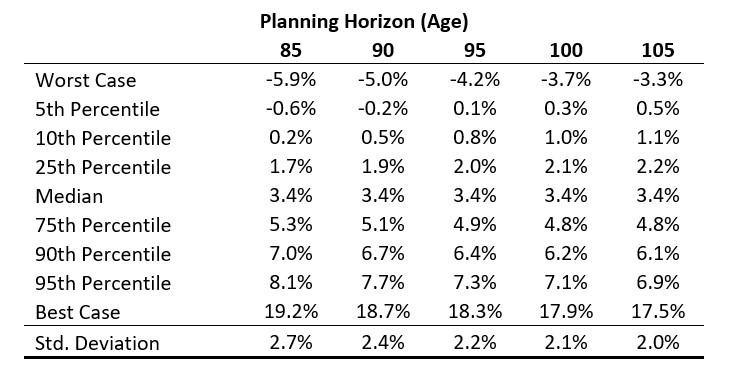

Exhibit 1.2 presents the implied compounded actual returns for various planning horizons and possibilities of success. As these are actual return components, they’d help inflation adjusted spending. The arithmetic common portfolio return is 4 p.c actual with a typical deviation of 10 p.c. Nonetheless, for deciding on a set return assumption, one should account for the chance of success they search for the spending plan by way of each a planning horizon and chance of success. As an illustration, if the retiree sought a 90 p.c likelihood that portfolio distributions might be sustained by means of age ninety, this may suggest an assumed fastened actual progress price for the portfolio from the tenth percentile of outcomes at 0.5 p.c.

Exhibit 1.2 Fastened Charges of Return Assumptions for a Sixty-5-Yr-Previous Reverse Engineered Inflation-Adjusted Compounded Returns for Retirement

Supply: Personal calculations with 100,000 Monte Carlo Simulations for a 50/50 portfolio of shares and bonds. These calculations are based mostly on the web portfolio returns proven in Exhibit 3.11. The portfolio’s actual arithmetic return is 4% and normal deviation is 10%.

We should always make just a few observations about this 0.5 p.c return worth. First, it’s lower than the assumed 1 p.c actual return from holding bonds. In different phrases, to realize the specified success price from the diversified portfolio, one finally ends up assuming a decrease return, and due to this fact a decrease spending quantity, than bonds might guarantee. The flip aspect of this, although, is that 90 p.c of the time the retiree might anticipate to earn a better efficient return than this quantity and will even have the ability to develop their wealth all through retirement as they in any other case are spending lower than would have been possible. Conversely, the bond ladder would lock-in the 1 p.c actual return all through retirement with out a likelihood for upside.

The opposite fascinating facet is to notice that the fastened return assumption will increase for longer retirement horizons, as it’s 0.8 p.c for planning by means of age ninety-five and 1 p.c (matching the bond yield) for planning by means of age 100. The explanation that returns improve with the time horizon is as a result of to maintain spending for longer, the spending quantity should lower, which reduces the impression of sequence-of-returns danger.

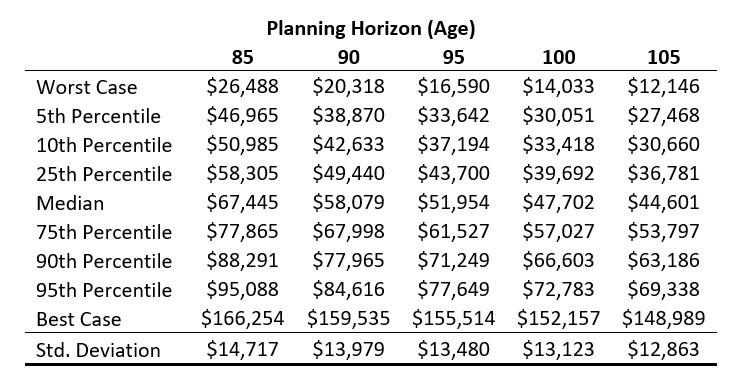

This idea is seen extra clearly in Exhibit 1.3, which gives the corresponding spending numbers for the returns within the earlier exhibit. Returning to the identical instance, if the retiree seeks a 90 p.c likelihood that spending lasts to age ninety, they’d select from the tenth percentile of spending outcomes. That’s $42,633 of annual inflation-adjusted spending. To maintain spending by means of age ninety-five with the identical success price, spending would wish to scale back to $37,194. It is a 3.72 p.c withdrawal price from retirement date belongings, and it might be the quantity that corresponds to the 4 p.c rule-of-thumb with these market expectations for a thirty-year retirement. If sustainability with 90 p.c success was as a substitute hunted for thirty-five years by means of age 100, then the annual spending quantity falls additional to $33,418. Once more, it’s as a result of the spending quantity decreases that the return assumption can improve; the decrease spending price reduces the publicity to sequence-of-returns danger and reduces the impression of funding volatility within the retirement plan.

Exhibit 1.3 Sustainable Spending for a Sixty-5-Yr-Previous with $1 Million of Belongings Reverse Engineered Inflation-Adjusted Sustainable Spending Quantities for Retirement

Supply: Personal calculations with 100,000 Monte Carlo Simulations for a 50/50 portfolio of shares and bonds. These calculations are based mostly on the web portfolio returns proven in Exhibit 3.11. The portfolio’s actual arithmetic return is 4% and normal deviation is 10%.

That is an excerpt from Wade Pfau’s ebook, Security-First Retirement Planning: An Built-in Method for a Fear-Free Retirement. (The Retirement Researcher’s Information Collection), available now on Amazon

{kind=link}