Image this situation: 18 years in the past — for those who had been fortunate to have thought of it — you began a university financial savings account in your little one who’s now graduating from highschool.

The previous two years have been a whirlwind of campus visits and functions. All of this work resulted in a thick envelope delivered to the brink of your property. Contained in the envelope, your little one finds out they’ve been accepted, and also you rapidly be taught simply how shut (or not shut) the varsity’s cost-of-attendance net price calculator is to your state of affairs.

As the joy settles and you start planning for the following chapter, the truth of upper training prices may be overwhelming. Let’s discover strategic choices like Mother or father PLUS Loans and PSLF, together with 529 financial savings to assist ease the burden.

School prices hit report highs over the a long time

School training prices at the moment have skyrocketed for the reason that Nineties. In accordance with School Board’s annual Trends in College Pricing report, from 1992-93 to 2022-23 tutorial years, common printed tuition & charges for:

- 4-year public universities elevated from $4,870 to $10,940.

- 4-year non-public nonprofit school elevated from $21,860 to $39,400.

The above figures don’t embrace room and board, allowances for books and provides, transportation and different private bills. The geographic location of an academic establishment would possibly drive a big piece of those prices, however the annual additional prices to think about might simply be one other $15,000 to $20,000 per yr.

Simply think about what it prices to take care of a one-bedroom house in a metropolis and canopy bills for meals over the course of a yr.

The common inflation-adjusted price of training has gotten twice as costly since your technology went to school. Add in 4 years of faculty for one little one to the above numbers, and you may be a mean bar tab (kidding) that ranges from $100,000 to $240,000.

Let’s additionally not neglect that averages are averages. The precise price of training finally ends up in your door’s threshold simply months earlier than your little one begins their first semester of faculty.

Is a 529 school financial savings plan the best choice?

So how do you put together for this unknown, seemingly very excessive, expense?

Historically, you’d fill the prices within the following order:

- Scholarships acquired and/or grants awarded.

- Federal support in your little one’s title.

- A mixture of the 529 School Financial savings Plan and your money.

However let’s put aside the primary two above, and as a substitute, contemplate professional replacements for the third answer.

You (the mum or dad) work for the school your little one attends. | You’re employed for a university affiliated with the varsity your little one attends. | You’re employed for any nonprofit 501(c)(3) group, federal employer, or state employer and pursue PSLF after commencement, using double consolidation. |

Consequence: Free Tuition & Charges, and presumably Room & Board | Consequence: Similar as Possibility A, at finest. | Consequence: Low funds throughout reimbursement time period, and your remaining loans are forgiven. |

Possibility A and Possibility B take superior planning. Normally, dad and mom who’re professors make the most of these two choices and primarily work for the college for different causes (i.e., analysis alternatives, tenure, and so forth.). Moreover, there’s a danger that their little one actually needs to attend school elsewhere.

Possibility C is just not essentially a tried and examined path, however it’s one thing to think about for fogeys who haven’t had the chance to avoid wasting for one thing they couldn’t have anticipated would double in worth or just didn’t have the means to avoid wasting alongside the way in which.

Maximizing your funds with Mother or father PLUS Loans

In the case of filling within the remaining price after scholarships, grants and federal support provided in your little one’s title, you may be gazing a six-figure or a number of six-figure monetary dedication. In case you deal with learn how to pay for it with loans, the Division of Schooling provides Mother or father PLUS Loans to fill that hole.

Mother or father PLUS loans are, on the floor, costly loans. Like different Direct PLUS Loans from the Division of Schooling, they arrive with an almost 4% origination charge and are at all times 1.0% increased than federal loans in your little one’s title.

However the quantity you borrow in your little one’s training (assume $20,000 to $60,000 yearly) is normally a lot increased than the quantity that’s provided to your little one (someplace between $5,500 to $7,500 yearly).

When your little one receives a monetary support bundle from their undergraduate establishment, it might very simply look one thing like this:

Whole price of annual attendance: $65,000

- Benefit-based scholarship: $8,000

- Grants: $0

- Direct Stafford Backed Loans: $2,000

- Direct Stafford Unsubsidized Loans: $3,500

In order that signifies that the first semester complete is $32,500:

- Benefit-based scholarship: $4,000

- Grants: $0

- Direct Stafford Backed Loans: $1,000

- Direct Stafford Unsubsidized Loans: $1,750

Quantity due September fifteenth, this yr: $25,750

So quick ahead to the tip of eight semesters. In case you took out Mother or father PLUS Loans underneath one mum or dad’s title for the above quantity, then you definately’d have $206,000 of mortgage debt, plus accrued curiosity — maybe a complete of $250,000.

Seeing a quantity like that may be alarming — particularly if that quantity multiplied by eight semesters — isn’t sitting in your little one’s School Financial savings 529 Plan. The quantity due can normally be paid in installments, however 4 months later, one other installment plan would begin for the following semester.

Compound this with two kids who overlap in school years, and the state of affairs simply received doubly troublesome to maintain up with!

As an alternative, contemplate this four-step technique:

- Borrow Mother or father PLUS Loans. A mum or dad who works for, or is planning to work for, a PSLF-qualifying employer and/or has a decrease earnings, can settle for Mother or father PLUS Loans to pay the stability due every semester. NOTE: For forgiveness functions, “sharing” the Mother or father PLUS Mortgage burden between two spouses isn’t an amazing concept. Choose one mum or dad and put the entire loans of their title alone.

- Work for a qualifying employer. Plan to work for – for those who don’t already – a qualifying employer for the PSLF program by the point your little one graduates school.

- Reap the benefits of double consolidation. Consolidating your Mother or father PLUS Loans offers you entry to solely the Revenue-Contingent Reimbursement plan. The double-consolidation loophole allows you to entry a higher number of income-driven reimbursement plans that may cut back your funds to solely 10% of your discretionary earnings.

- Work towards Public Service Loan Forgiveness (PSLF). Pursue a 120-month PSLF monitor on an income-driven reimbursement plan, and get your remaining stability forgiven tax-free.

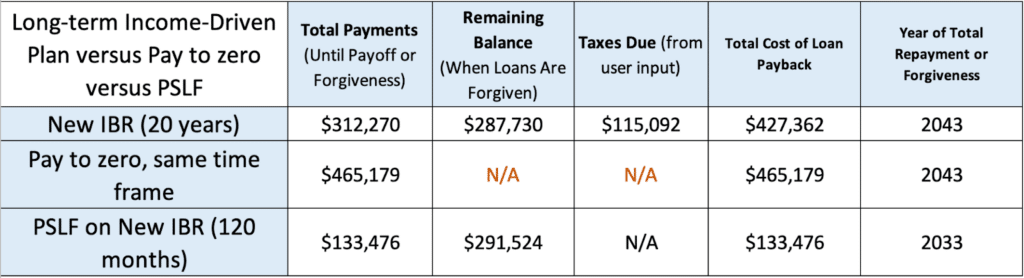

In case your earnings as a mum or dad family (let’s use a household measurement of two) had been $150,000 per yr, then your month-to-month fee on an income-driven reimbursement plan, reminiscent of the brand new Revenue-Primarily based Reimbursement (new IBR) plan, could be about $1,000 monthly.

In case your family earnings will increase by 3% per yr, then your recalculated month-to-month funds would improve each 12 months as nicely. Under is a breakdown of what you’d find yourself paying for those who continued making these funds all through the 20-year new IBR time period:

Evaluate the income-driven reimbursement plan to the “pay to zero” path (similar rate of interest, similar timeline) and it comes out forward, on paper.

In case you labored a W-2 job, full-time, for a qualifying employer that qualifies underneath PSLF, then you may shortcut your timeline for forgiveness. After 120 months of funds made on any income-driven reimbursement plan — persevering with to make use of the brand new IBR plan for example — it might look one thing like this:

So by month 120, you’d find yourself paying about $133,000 in complete month-to-month funds, with a projected $291,500 stability forgiven that’s NOT taxable on the federal degree.

Observe: You would possibly pay state earnings tax, so it’s a good suggestion to earmark financial savings for this.

All in all, there’s a fairly good case for the price of training with a PSLF end result. The important thing components embrace one mum or dad borrowing Mother or father Plus loans, the identical mum or dad’s employer being a certified employer for PSLF functions, and family earnings.

Many of the income-driven plans let the mum or dad borrower exclude their partner’s earnings in the event that they file as “married, submitting individually.” Additionally, with the proposed Biden IDR plan, the numbers above look rosier for the PSLF end result. It proposes a decrease drop for the household poverty guideline which determines discretionary earnings percentages for undergraduate, versus PLUS Loans.

Widespread FAQ from single dad and mom

For single dad and mom, the maths for a forgiveness end result on an IDR plan is comparatively easy since family earnings is one and the identical. However let’s say that you’re a single mum or dad who has loans out of your previous training and are considering of including on Mother or father PLUS Loans.

For lots of mum or dad debtors who’ve loans from 15+ years in the past, it’s widespread to have taken out undergraduate Stafford Backed Loans, and undergraduate or graduate Stafford Unsubsidized loans which have since been consolidated.

Consolidated loans, and even loans saved as they had been, have a fee historical past. Some may need been on an IDR plan and a few may need been on a hard and fast or graduated reimbursement plan.

When you may have a reimbursement historical past on a mortgage and also you consolidate that mortgage with a Mother or father PLUS Mortgage or group of Mother or father PLUS Loans, the reimbursement historical past of your loans might add to the ensuing consolidated mortgage reimbursement historical past. However even when there’s reimbursement historical past on the Mother or father PLUS mortgage(s), that historical past is erased.

Traditionally, and (as of the writing of this), consolidation erases any and all reimbursement historical past on any loans. However that isn’t the case with the IDR waiver; additionally, going ahead past mid-2023, which may not be the case with consolidation.

With the IDR Waiver, the reimbursement historical past of your training loans could be counted towards reimbursement standing on an IDR plan for a newly consolidated mortgage that features Mother or father PLUS Loans. When the IDR waiver interval is over, the proposed remedy for consolidations is that new consolidations would take a weighted reimbursement historical past common of the underlying loans (these being consolidated).

Allow us to assist

The timeline of months that rely towards PSLF begins when your Mother or father PLUS Loans are in reimbursement. You probably have a number of kids in school, then an IDR plan fee is due for so long as the youngest of the loans is projected to finish in complete reimbursement or forgiveness. Though we predict it’s value a pre-debt consult to determine this out with only one little one, it goes with out saying {that a} pre-debt seek the advice of is value a paid dialog with a licensed pupil mortgage skilled when there are a number of kids set to attend school.

1Sallie Mae disclosures. Lowest APRs proven for Sallie Mae Loans: The borrower or cosigner should enroll in auto debit by Sallie Mae to obtain a 0.25 proportion level rate of interest discount profit. This profit applies solely throughout energetic reimbursement for so long as the Present Quantity Due or Designated Quantity is efficiently withdrawn from the approved checking account every month. It could be suspended throughout forbearance or deferment.

2Earnest: All charges listed above symbolize APR vary. Charge vary above

consists of non-compulsory 0.25% Auto Pay low cost. Earnest disclosures.

3Ascent disclosures. Disclosure: Ascent Pupil Loans are funded by Financial institution of Lake Mills, Member FDIC. Mortgage merchandise will not be out there in sure jurisdictions. Sure restrictions, limitations; and phrases and situations might apply. For Ascent Phrases and Circumstances please go to: www.AscentFunding.com/Ts&Cs. Charges are efficient as of 12/01/2022 and replicate an automated fee low cost of both 0.25% (for credit-based loans) OR 1.00% (for undergraduate outcomes-based loans). Computerized Cost Low cost is accessible if the borrower is enrolled in automated funds from their private checking account and the quantity is efficiently withdrawn from the approved checking account every month. For Ascent charges and reimbursement examples please go to: AscentFunding.com/Charges. 1% Money Again Commencement Reward topic to phrases and situations. Cosigned Credit score-Primarily based Mortgage pupil should meet sure minimal credit score standards. The minimal rating required is topic to vary and should rely on the credit score rating of your cosigner. Lowest APRs require interest-only funds, the shortest mortgage time period, and a cosigner, and are solely out there to our most creditworthy candidates and cosigners with the best common credit score scores.

{kind=link}