The housing market has been stubbornly irritating for potential house patrons.

Not solely have mortgage charges doubled over the previous 12 months, however house costs stay extremely elevated, regardless of some minor enhancements.

Certain, you would possibly hear that the housing market is crashing, or that we’re in a house value correction.

However that doesn’t imply an entire lot while you zoom out and take a look at house costs over the previous couple years.

What’s worse is regardless of abysmal affordability, house costs might not even come down.

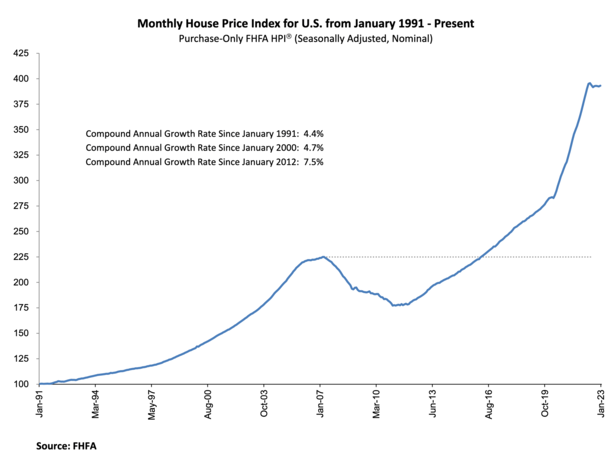

Dwelling Costs Are Up 5.3% From a 12 months In the past

Whereas there have been declines in sure overheated metros nationwide, house costs are up 5.3% nationwide from January 2022 to January 2023.

That is in keeping with the newest Federal Housing Finance Company (FHFA) seasonally adjusted month-to-month Home Worth Index (HPI).

And so they rose 0.2% in January from a month earlier after registering a 0.1% month-to-month value decline in December 2022.

If we drill in a bit extra, wanting on the 9 census divisions, seasonally adjusted month-to-month house costs from December 2022 to January 2023 confirmed a wider vary.

Dwelling costs have been off 0.6% within the Pacific division and up 2.0% within the New England division.

On a 12-month foundation, costs have been -1.5% within the Pacific division and +9.6% within the South Atlantic division.

As I all the time say, actual property is native, and that is very true nowadays with some markets in several phases than others.

However simply take a look at the nationwide house value chart above. Dwelling costs have completely surged over the previous few years.

And so they pulled again by a tiny quantity earlier than flattening out. The takeaway is that house costs are excessive and won’t come down a lot.

Dwelling Costs Haven’t Fallen A lot As a result of Stock Stays Tight

Regardless of frothy house costs and questionable, speculative shopping for from buyers, house costs have held up fairly effectively.

When you’re that house value chart and questioning how on earth costs may be effectively above ranges seen in 2006-2008, blame stock.

There’s been a severe lack of properties on the market for a few years now, exacerbated by the mortgage price lock-in impact.

In brief, a lot of right now’s owners have 30-year fixed-rate mortgages which are priced between 2-4%.

Additionally referred to golden handcuffs (assuming they need to promote/transfer), these low charges make it very tough to half with the property.

Even when they’re able to afford a subsequent house buy, they could be turned off by the brand new rate of interest set at 6%.

This explains why the stock of unsold present properties was a mere 980,000 on the finish of February, per the National Association of Realtors.

That’s simply 2.6 months’ provide on the present month-to-month gross sales tempo. And as we all know from provide and demand, when provide is low and demand is excessive, the value goes up.

For the file, the median existing-home value fell 0.2% in February to $363,000, ending 131 consecutive months of year-over-year will increase, the longest in historical past.

So there’s some downward strain on house costs, however 0.2%? That’s not going to do a lot is it?

How A lot Revenue Is Required to Purchase a Dwelling At the moment?

The rule of thumb for housing prices is about 28% of your gross income. So for those who make $80,000, not more than $1,867 can go towards the mortgage.

That features principal and curiosity, property taxes, owners insurance coverage, and PMI and HOA dues if relevant.

The issue is the typical United States house worth is $327,514, per Zillow, and is up 6.8% over the previous 12 months.

The true median family earnings within the U.S. was $70,784 in 2021, and really declined since 2019 on account of inflation.

If we contemplate a $325,000 house buy with a 20% down payment we arrive at a $260,000 mortgage quantity.

We’ll throw a 6% mortgage rate to reach at a P&I cost of $1,558.83. Now let’s add taxes of $340 monthly and owners insurance coverage of $100 monthly.

That takes us to roughly $2,000 monthly, or about 34% of that $70,784 median earnings.

It’s not horrible, however it’s nonetheless above the 28% rule of thumb for a housing cost. And that’s utilizing favorable math.

If it’s a 5% or 10% down cost, you’ll have PMI, the next mortgage price, and a bigger mortgage quantity to deal with.

So it’s fairly clear that house costs are unaffordable for many at their present ranges. However with no significant addition of stock, issues received’t change.

And as famous, many present homeowners aren’t going anyplace. The one sport on the town is newly-built properties, however builders can solely construct a lot.

Moreover, new builds usually aren’t situated in densely-populated areas the place there’s a larger want for brand new, inexpensive housing.

In California, simply 21% of all residents earned the minimal earnings wanted to buy an $822,320 median-priced house in 2022, down from 27% in 2021, per CAR.

It was barely higher nationwide, with 43% in a position to afford a median $392,800 property.

What Occurs Subsequent for Dwelling Costs?

Black Knight noted that house costs rose 0.16% in February after seven consecutive month-to-month declines.

It was the strongest single-month achieve since Could 2022, although at 1.94%, annual house value progress dipped under 2% for the primary time since 2012.

This helps the thesis that house value progress was going to gradual, aka decrease year-over-year house value features.

However that precise, falling house costs would nonetheless be laborious to return by. And now that we’re getting into the spring house shopping for season, house costs might truly re-accelerate.

Mortgage charges simply occur to be falling too, with the 30-year again to its February low of round 6.125%.

Charges have been about 1% increased in early March, so there could be some severe tailwinds for the housing market, not less than by way of house value trajectory.

Sadly, this implies it’s going to stay tough to buy a house with median earnings. And that though house costs are overpriced, they could stay that approach for the foreseeable future.

In the end, we might face years of comparatively flat house value progress, which might nonetheless put homeownership out of attain for a lot of.

In fact, there are affordability options coming to market, whether or not it’s the California Dream For All loan, or temporary rate buydowns.

For these hoping for or anticipating a housing crash, you’ve obtained to have a look at the basics. It’s not 2008 though house costs are considerably increased.

The mortgages are a lot completely different and housing provide is so much decrease. Till that adjustments it’d be laborious to attract too many parallels.

Learn extra: What will cause the next housing crash?

{kind=link}