The temporary’s key findings are:

- Many consultants favor full prefunding of state and native pensions to take care of fiscal sustainability, which implies huge contribution hikes.

- This evaluation explores an alternate: stabilizing pension debt as a share of GDP.

- Beneath present contribution charges, baseline projections present no signal of a significant disaster within the subsequent 20 years even when asset returns are low.

- But, many plans can be in danger over the long run of exhausting their belongings, so motion can be wanted.

- Plans can attain a sustainable footing by stabilizing their debt-to-GDP ratio, with a lot smaller contribution hikes than beneath full funding.

Introduction

State and native authorities pension plans are vital financial establishments in the US. They maintain practically $5 trillion in belongings; their annual funds to beneficiaries are equal to about 1.5 % of nationwide GDP; and over 11 million beneficiaries depend on these funds to assist themselves in retirement. In recent times, consideration has centered on the plans’ giant unfunded liabilities and the necessity to absolutely fund these obligations. However is full funding the one solution to obtain fiscal sustainability?

This temporary, which relies on a current paper, explores an alternate path to the fiscal sustainability of state and native pension plans – particularly, stabilizing their pension debt as a share of the financial system. To evaluate the feasibility of this method requires: 1) projecting the annual money flows for a nationally-representative pattern of 40 state and native pension programs to see the long run evolution of every plan beneath present contribution ranges; and a couple of) estimating the contribution will increase wanted to stabilize the ratio of pension debt to the financial system.

The dialogue proceeds as follows. The primary part supplies background on the fiscal stability of state and native plans. The second part describes the information and methodology. The third part presents the outcomes for when plans will exhaust their belongings beneath present funding ranges and profit provisions. A key discovering is that pension advantages, as a share of the financial system, are at the moment close to their peak and can decline considerably over time because of the reforms instituted by many plans. Nonetheless, many plans are in danger over the long run of exhausting their belongings, so motion can be wanted. The fourth part presents the outcomes on the choice path, particularly the contribution adjustments required to stabilize pension debt, each in the long term and to get the ratio on the finish of 30 years again to at this time’s degree.

The ultimate part concludes that the US is just not going through a state and native pension disaster however, over the long run, a big share of plans face the chance of insolvency. Therefore, they would wish to extend contributions to attain sustainability. However the required changes to stabilize debt relative to the financial system are typically reasonable in dimension and, in all circumstances, considerably decrease than the changes required beneath the standard full prefunding framework.

Background

In recent times, public pension analysts have centered intensely on the necessity for full prefunding of state and native pensions. The method would allow a plan to close down at any time and pay full advantages with out further contributions. This emphasis on full funding is a comparatively new growth. As just lately as 2008, many analysts thought-about a funding ratio of 80 % to be sound apply for state and native plans. However teachers and policymakers have embraced the total funding aim with gusto.

In tutorial work, some researchers explicitly state that full prefunding is the right aim for plans, whereas others make the argument implicitly by focusing evaluation on the fiscal prices of transitioning to full funding. With regard to policymakers, CalPERS, the nation’s largest state and native pension plan, explicitly advocates for full funding, stating that the “best degree” of prefunding is one hundred pc. Alongside related strains, a blue ribbon panel commissioned by the Society of Actuaries “wholeheartedly believes that…plans must be pre-funded.” Lastly, rankings companies sometimes view “underfunding of pension…advantages as [a] key credit score problem.”

But, full prefunding is just not the one solution to make a pension system sustainable.

Different papers deal with the prices of not prefunding: uneven info between authorities staff and different voters over the price of pensions could enable authorities staff to accrue rents within the absence of prefunding (Bagchi 2019 and Glaeser and Ponzetto 2014); and unfunded pensions could decrease the capital inventory (Feldstein 1974). Lastly, Lucas (2017) supplies a radical dialogue of each the uncertainty surrounding optimum funding ranges for state and native pensions, in addition to arguments for and towards full funding. Certainly, even an unfunded pay-as-you-go program with a devoted earnings stream – resembling Social Safety – can honor obligations with out recourse to further funding so long as the inner charge of return paid to beneficiaries doesn’t exceed the expansion charge of the wage base. In fact, pay-as-you-go applications can face shortfalls if demographic adjustments enhance the expansion in outlays or decrease the expansion of revenues. Nonetheless, mature, partially funded programs, resembling state and native pension plans, which have accrued belongings to offer a buffer, can stay sustainable even within the face of adversarial shocks.

Extra broadly, unfunded pension liabilities are merely a type of authorities debt. Such public debt may be sustainable so long as the federal government makes acceptable service funds on it. The requirement for holding pension debt secure relative to the financial system will depend on the connection between the expansion charge of the financial system (g) and the rate of interest (r). If r = g, then the required annual contribution to the pension fund is just the traditional value – the price of advantages accrued in a given 12 months. When the speed of curiosity is bigger than the expansion charge of the financial system, r > g, contributions must be enough to cowl the traditional value and debt service prices. If r < g, then debt may be held fixed as a share of the financial system with contributions lower than the traditional value. Whereas the required contribution charge depends on the assumed relationship between r and g, the important thing level is that sustainability doesn’t require full funding – stabilizing pension debt as a share of the financial system ought to enable the federal government to fulfill all its pension obligations with out crowding out different public companies.

Furthermore, transitioning to full funding entails generational transfers – with present generations paying greater taxes/having decrease advantages with a purpose to scale back taxes/increase advantages on future generations. Stabilizing the extent of funding is a means of equalizing burdens throughout generations.

Information and Methodology

The premise for the evaluation is projecting the long run circulation of advantages for state and native pension plans. The principal supply for these calculations is the Public Plans Database (PPD) maintained by the Heart for Retirement Analysis at Boston School. The PPD accommodates plan-level knowledge accounting for 95 % of state and native plan membership and belongings in the US. This evaluation makes use of a pattern of 40 plans, which incorporates the most important 20 public pension plans and an extra 20 chosen in order that the pattern matches the nationwide PPD pattern when it comes to funding, budgetary, and demographic traits.

For the person state and native plans within the pattern, further info comes from the plan’s actuarial valuations and the state’s Complete Annual Monetary Stories for FY 2017.

Annual pension advantages are sometimes equal to the years of service multiplied by ultimate common wage instances the profit issue. Thus, the profit issue is the proportion of ultimate wage to which a pension beneficiary is entitled for annually of service. Sometimes, the typical wage from the very best three to 5 years is used to find out the ultimate wage.

The methodology may be divided into three phases. The primary stage entails estimating the long run circulation of profit funds to present beneficiaries and staff. This course of requires utilizing mortality tables to age the preliminary distribution of present beneficiaries annually and details about their pension advantages by age to calculate annual profit funds. For present staff, the method entails getting old the workforce annually (incrementing years of service and age) and utilizing the chances of retirement, incapacity, loss of life, and quits or termination by age and years of service to create a matrix of recent beneficiaries by 12 months. Data on pension eligibility, profit formulation, and financial assumptions is then used to calculate the pension obligations for these new beneficiaries by 12 months. Projections are checked towards the liabilities reported within the related actuarial valuations. Then, the money flows are re-estimated utilizing constant financial assumptions – nominal wage progress of three.4 % and CPI inflation of two.2 %. Though these procedures are conceptually fairly simple, the precise implementation may be very advanced.

The second stage entails projecting plan membership progress to estimate advantages for future staff. New hires in annually are set equal to the earlier 12 months’s head depend multiplied by the sum of the projected progress charge within the authorities’s workforce and the proportion of withdrawals and retirements from the workforce within the earlier 12 months. Projected workforce progress retains fixed the ratio of the federal government workforce to the working-age inhabitants. An additional assumption is that the age distribution and relative salaries of recent hires match the distribution of present staff with fewer than 5 years of service. Every group of recent hires then produces a brand new stream of advantages beginning at every future 12 months, with the worth of these future advantages calculated in precisely the identical means as they had been for the present lively staff however adjusting for adjustments to plan provisions instituted for brand new hires.

The ultimate stage requires pairing the profit money circulation projections with info on asset ranges and assumed future returns to evaluate the fiscal outlook for every plan. For plan belongings, the place to begin is PPD knowledge for FY 2017, however asset values modified considerably between FY 2017 and FY 2021, so the values are up to date for our evaluation.

Since then, after we accomplished the research on which this temporary relies, mixture plan belongings have fallen about 20 %, which aligns with the roughly 20-percent drop in equities over the identical interval. Decrease asset ranges make acheiving any funding aim (e.g. full prefunding or stabilizing pension debt as a share of the financial system) tougher.

To calculate future asset ranges, the evaluation assumes three different actual charges of return.

- The bottom – 0.5 % – is roughly equal to the longer-run risk-free charge lately, as mirrored by the yield on the zero-coupon 20-year Treasury Inflation Projected Securities.

- The intermediate assumption – 2.5 % – is equal to the return on a combined portfolio containing 60 % risk-free belongings and 40 % equities.

- The best – 4.5 % – displays the anticipated return on a pension portfolio comprised of 20 % risk-free belongings and 80 % equities.

An vital problem is whether or not funding returns on pension belongings ought to be risk-adjusted in authorities finances projections. Such an adjustment would forestall plans from showing more healthy just because they put money into riskier belongings. This problem is tough and contentious. The Congressional Price range Workplace, for instance, makes use of a risk-free charge of return for applications like scholar loans in its “Honest Worth” method, however makes use of anticipated returns in its finances accounting.

In all circumstances, plan liabilities on this evaluation are calculated by discounting promised advantages by the 0.5-percent actual risk-free charge. This method incorporates the idea that pension obligations can be paid out in full in practically all future states of the world. This assumption is unlikely to be strictly true, which makes it conservative. In any case, the outcomes aren’t very delicate to the chosen low cost charge as a result of the main target is the steadiness of pension debt somewhat than its degree. In distinction, workouts that calculate what’s required for plans to be absolutely funded are very delicate to the assumed low cost charge on liabilities.

Outcomes: Outlook with Present Contributions

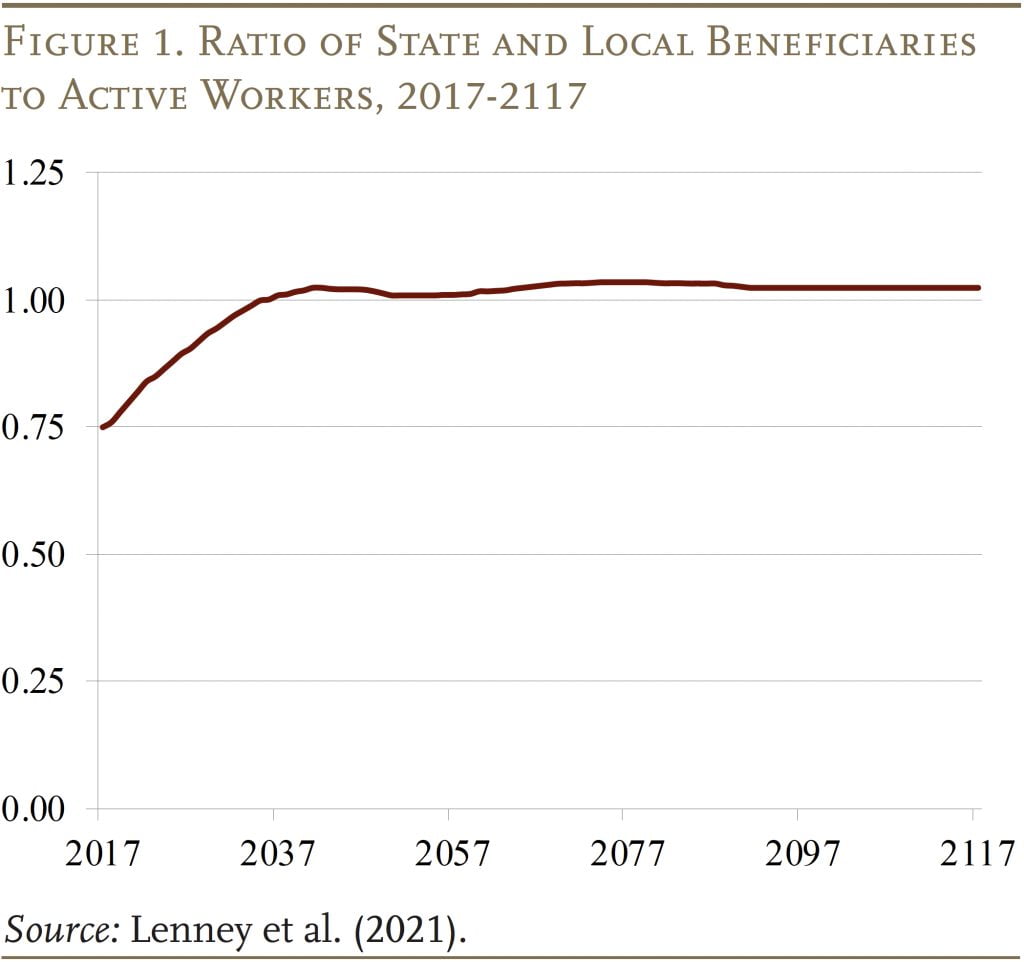

The projections produced 4 main findings. The primary is that the ratio of beneficiaries to staff in state and native governments is projected to extend about 36 % from 2017 to 2040 after which roughly stabilize (see Determine 1). This discovering is in keeping with projections by the Social Safety actuaries, which present that the ratio of Social Safety beneficiaries to staff is projected to rise about 39 % over this time interval. This similarity presents some assist that the long run circulation of state and native authorities staff has been appropriately modeled.

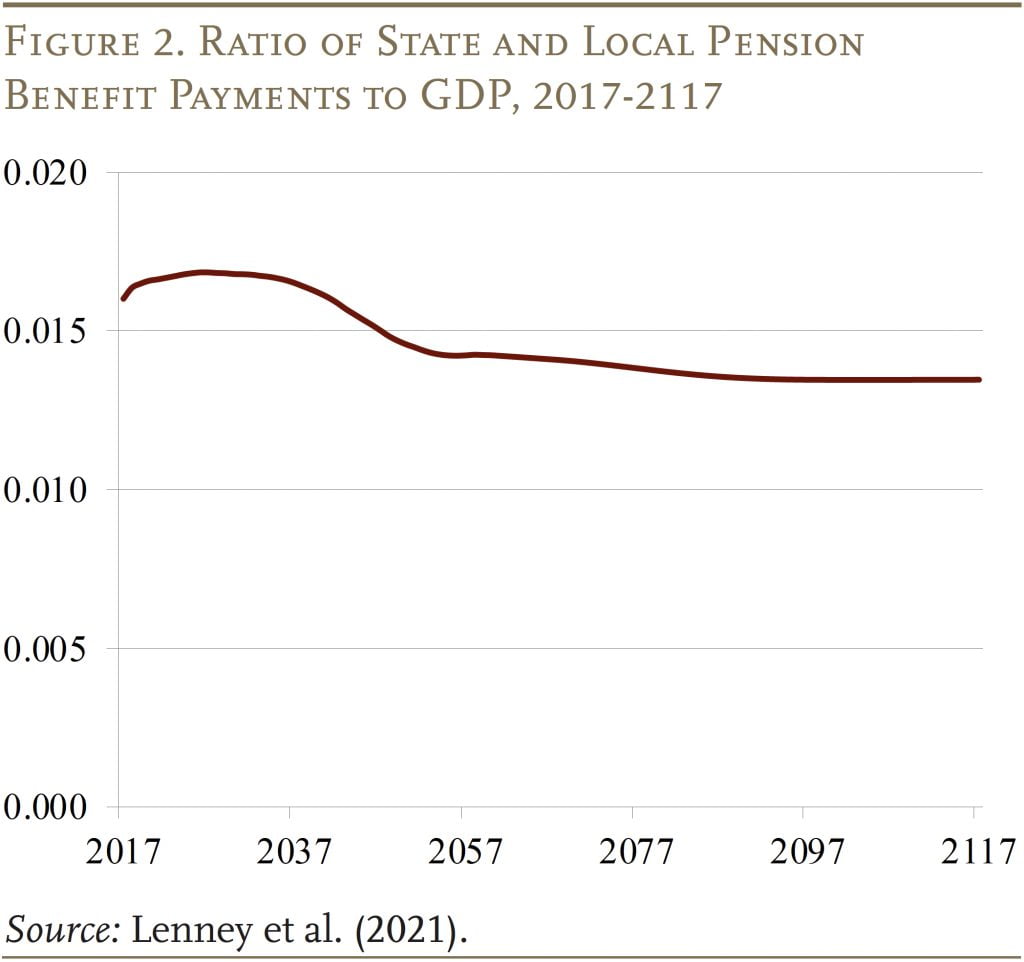

The second discovering is that, regardless of the rising ratio of beneficiaries to staff, annual profit funds as a share of the financial system is already close to its peak (see Determine 2). This stunning end result may be attributed to 2 elements. First, most pension plans don’t absolutely index their retiree advantages for inflation, which lowers the true worth of common advantages over time. Second, pension plans have steadily been making adjustments to decrease advantages and lift retirement ages for brand new hires. The lowered progress in common advantages because of the COLA restraints and new rent reforms offsets a big share of the results of the 36-percent progress within the ratio of beneficiaries to staff.

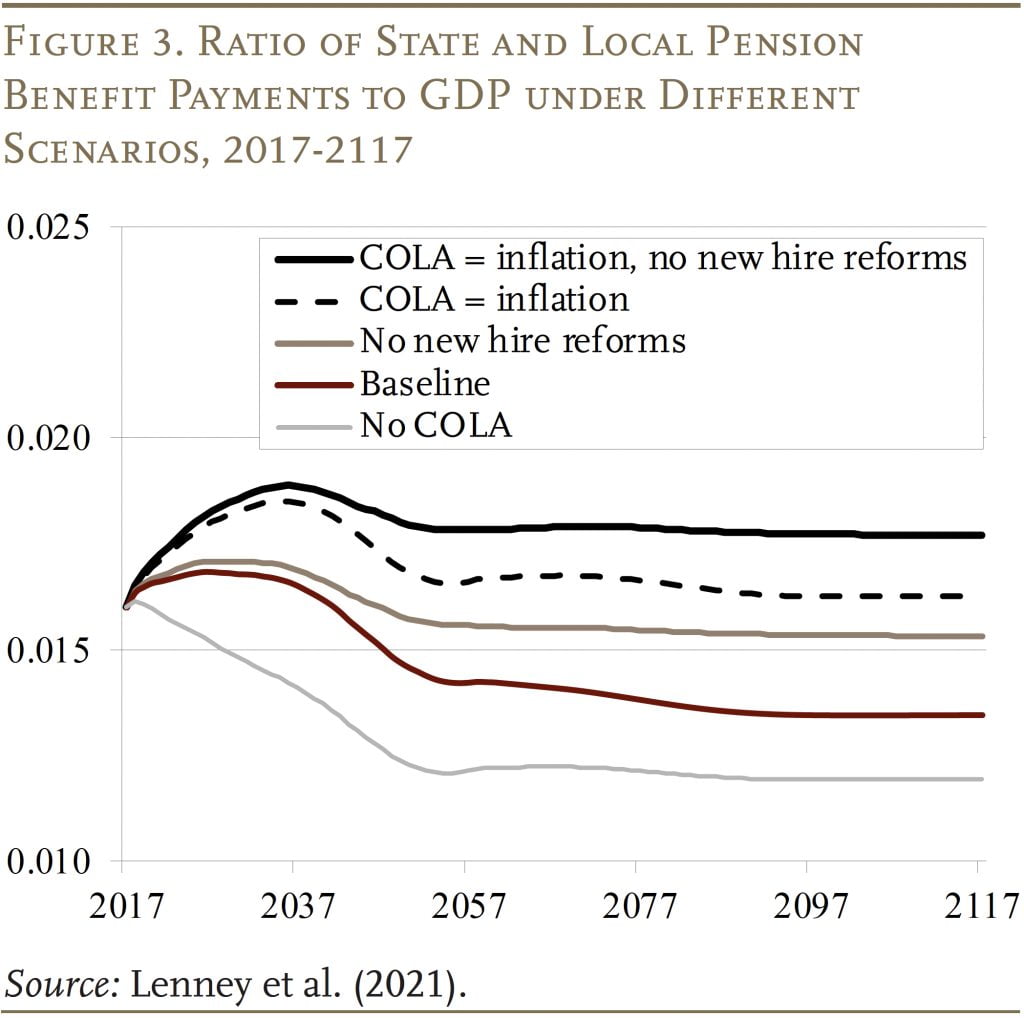

To drive the purpose house relating to the discrepancy between the sample for beneficiaries/staff and advantages/GDP, Determine 3 paperwork the affect of fixing assumptions about COLAs and new rent reforms. The highest line, which assumes a full COLA and no profit reductions for brand new hires, exhibits the identical rising sample evident within the ratio of beneficiaries to staff. Subsequent strains present the affect of incorporating the brand new rent reforms into the projections.

The truth that pension advantages as a share of payroll are, in mixture, close to their highest degree anticipated over the following few many years is a vital discovering for understanding the sustainability of state and native funds and the power of plans to easy by this era.

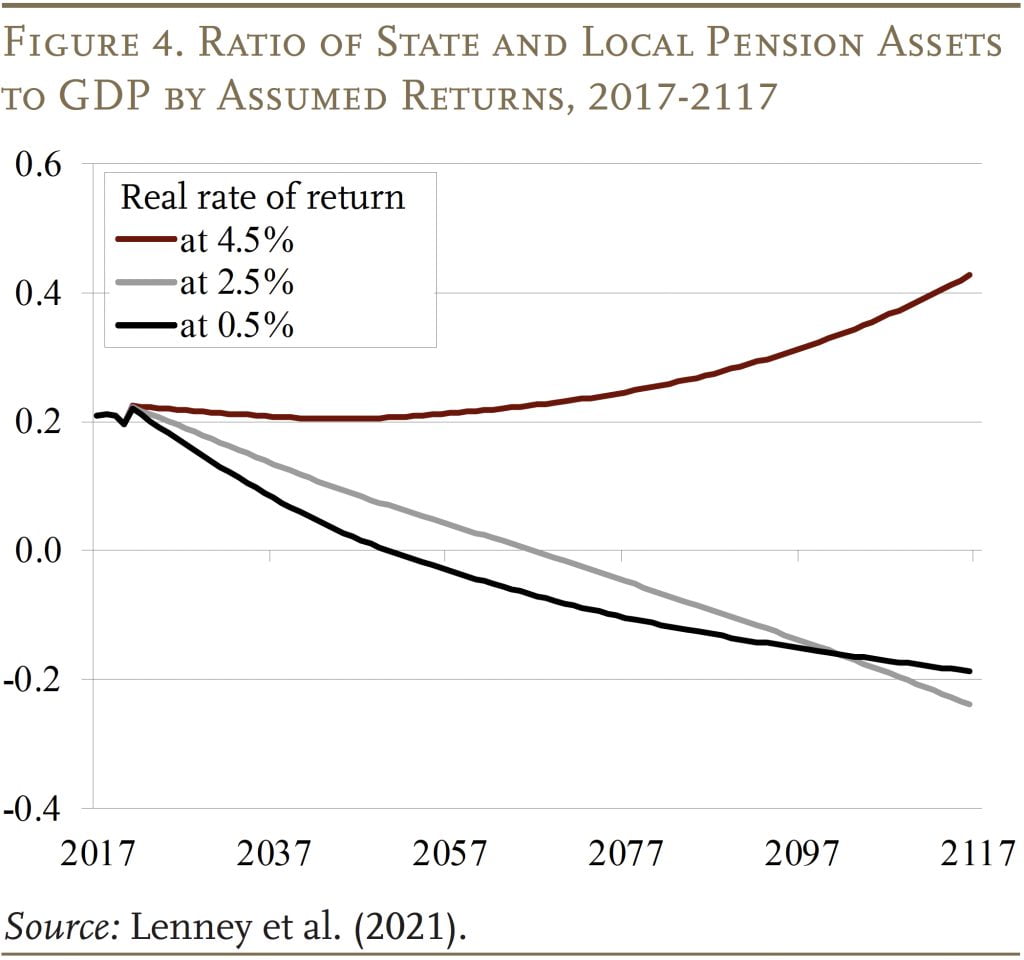

The third discovering on this present coverage evaluation pertains to the paths for belongings, relative to the financial system, beneath the three asset return assumptions (see Determine 4). Summing throughout the plans, with the 0.5-percent actual charge of return, present contributions are inadequate to maintain the plans solvent. Regardless of the projected decline in advantages relative to GDP, belongings relative to GDP start declining instantly and are exhausted in about 30 years. With a 2.5-percent charge of return, belongings are declining, however not as shortly; they’re exhausted in 47 years. In distinction, if plans earn 4.5 % on their belongings, they’re sustainable: at present contribution charges, belongings rise indefinitely and the plans face no fiscal stress.

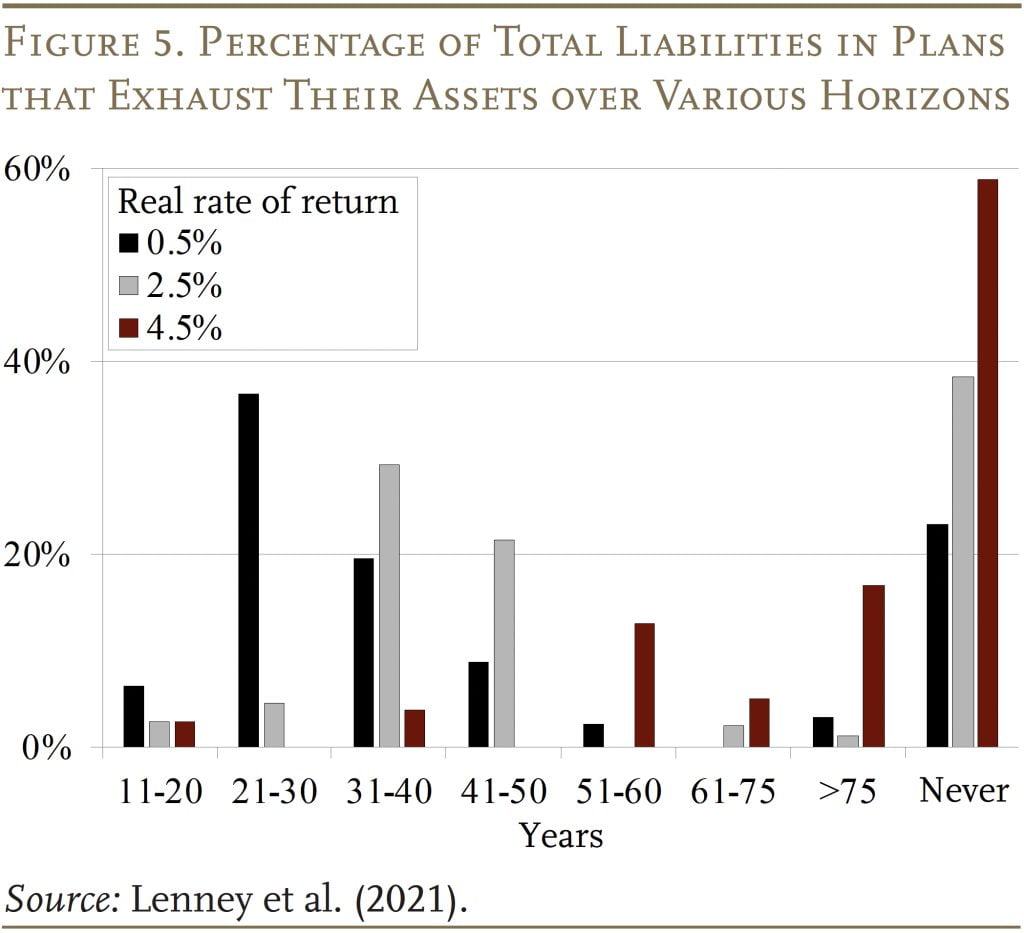

In fact, wanting on the exhaustion of pension belongings for the system as an entire masks plenty of variation throughout plans. Determine 5 exhibits the share of liabilities in plans that exhaust inside numerous time durations. With a 0.5-percent actual charge of return, about 6 % of liabilities are in plans that exhaust inside 20 years and 43 % are in plans that exhaust inside 30 years; even at this low charge of return, 23 % of liabilities are in plans that by no means exhaust. At a 2.5-percent actual return, solely 7 % of liabilities are in plans that exhaust throughout the subsequent 30 years, and 38 % are in plans that by no means exhaust. With a 4.5-percent actual return, virtually 60 % of liabilities are in plans that by no means exhaust, whereas the opposite plans do exhaust, however largely not for a lot of many years.

The message from these workouts is that almost all of plans don’t face an imminent disaster within the sense that they’re prone to exhaust their belongings throughout the subsequent 20 years. However a sizeable share may exhaust their belongings inside 30 years beneath the low-return state of affairs. And even beneath the high-return state of affairs, greater than 40 % are vulnerable to depleting their belongings over longer time horizons. Thus, changes can be obligatory. The questions are: How giant are these changes? and How pressing are they?

Outcomes: Pension Debt Stabilization

This evaluation entails estimating the adjustments in pension contributions required to stabilize pension debt relative to GDP. The primary train asks what everlasting adjustments within the contribution charge would make pension debt finally stabilize as a share of GDP. As a result of very long-run projections are inherently unsure, the second train asks what everlasting adjustments in contributions would get debt as a share of GDP again to at this time’s degree in 30 years.

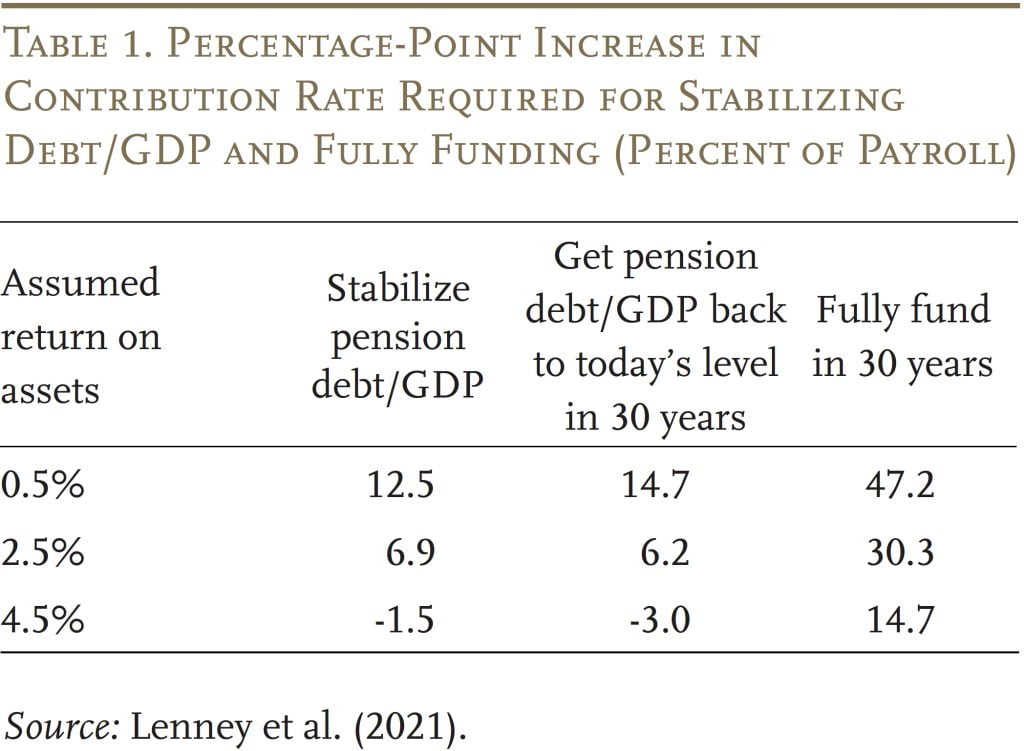

The outcomes of the simulations are proven in Desk 1. The required enhance within the contribution charge to stabilize the debt-to-GDP ratio is 12.5 share factors when belongings yield 0.5 %; 6.9 share factors with a return of two.5 %; and contributions could possibly be minimize with a return of 4.5 %. The numbers look very related with a aim of getting the debt/GDP ratio again to at this time’s degree in 30 years. To place these contribution adjustments into context, mixture pension contributions elevated by 10 share factors between 2009 and 2019. The ultimate column exhibits that the required percentage-point enhance in contribution charges to totally fund these plans could be 4 or 5 instances bigger. In fact, outcomes for all the state and native pension system hides substantial variation amongst plans (see Appendix).

The evaluation additionally produces some stunning outcomes. First, appearing sooner somewhat than later lowers the required enhance, however not by a lot. For instance, assuming belongings earn an actual charge of return of two.5 %, even when the plans do nothing for 30 years, the required enhance solely rises from 6.9 % to eight.6 % of payroll. When charges of return are assumed to be very low – particularly, lower than the expansion charge of the financial system – the contributions required to stabilize the debt are, after all, greater. However, strikingly, beneath this state of affairs, it is usually true that appearing sooner somewhat than later doesn’t assist. The instinct right here is that when rates of interest are lower than the expansion charge of the financial system, authorities debt has no fiscal prices.

The second stunning discovering is that the poorly funded plans aren’t those that must make the best contributions to stabilize. The reason being that these poorly funded plans have elevated their contribution charges considerably, made the most important cuts to advantages for brand new hires, and lowered their COLAs. Plans that made the most important adjustments in contributions since 2007 and the most important reforms to their advantages are at the moment contributing greater than sufficient to stabilize their debt, even at a 0.5-percent charge of return in lots of circumstances.

Conclusion

This temporary began by exploring the fiscal outlook for state and native authorities pension plans beneath present profit and funding insurance policies. The projections present no signal of an enormous pension disaster within the subsequent 20 years. Actually, regardless of the projected enhance within the ratio of beneficiaries to staff, profit funds as a share of the financial system are at the moment close to their peak and can finally decline considerably. In consequence, these plans may be placed on a sustainable footing – by stabilizing the ratio of pension debt to the financial system – with contribution charge will increase roughly equal to these adopted over the past 20 years.

Shifting the main target to reaching sustainability by sustaining a secure debt-to-GDP ratio from the extra typical emphasis on full prefunding deserves critical consideration. In an effort to prefund, state and native governments have elevated their pension contributions dramatically over the previous 20 years. These elevated contributions come at a big alternative value. Regardless of the lengthy financial growth that preceded the temporary COVID recession, provision of public items supplied by state and native governments remained depressed: actual per capita spending on infrastructure stood at about 25 % under its earlier peak, and state and native authorities employment per capita additionally remained properly under its earlier peak. Notably, a lot of this relative decline in state and native authorities employment occurred within the Ok-12 and better training sectors.

The analysis summarized on this temporary is actually not the final phrase on the subject. Certainly, different researchers have critiqued numerous features of the evaluation. However, persevering with with establishment or more and more stringent full-funding insurance policies additionally has prices. So, hopefully the fundamental concept offered here’s a first step in direction of constructing a extra sustainable framework for managing state and native pension plan liabilities.

References

Aubry, Jean-Pierre and Caroline V. Crawford. 2017. “State and Local Pension Reform since the Financial Crisis.” State and Native Plans Concern in Temporary 54. Chestnut Hill, MA: Heart for Retirement Analysis at Boston School.

Bagchi, Sutirtha. 2019. “The Effects of Political Competition on the Generosity of Public-Sector Pension Plans.” Journal of Financial Habits and Group 164: 439-468.

Blanchard, Olivier. 2019. “Public Debt and Low Interest Rates.” American Financial Assessment 109(4): 1197-229.

Bohn, Henning. 2011. “Should Public Retirement Plans Be Fully Funded?” Journal of Pension Economics and Finance 10(2): 195-219.

Boyd, Donald J. and Yimeng Yin. 2016. “Public Pension Funding Practices.” Albany, NY: Nelson A. Rockefeller Institute of Authorities.

California Public Workers’ Retirement System. 2014. Annual Review of Funding Levels and Risks, 2014. Sacramento, CA.

Costrell, Robert M. and Josh McGee. 2020. “Sins of the Past, Present, and Future: Alternative Pension Funding Policies.” Paper ready for the Municipal Finance Convention (July 13-14). Washington, DC: Brookings Establishment, Hutchins Heart on Fiscal and Financial Coverage.

D’Arcy, Stephen P., James H. Dulebohn, and Pyungsuk Oh. 1999. “Optimal Funding of State Employee Pension Systems.” Journal of Danger and Insurance coverage 66(3): 345-380.

Feldstein, Martin. 1974. “Social Security, Induced Retirement, and Aggregate Capital Accumulation.” Journal of Political Financial system 82(5): 905-926.

Glaeser, Edward L. and Giacomo A. M. Ponzetto. 2014. “Shrouded Costs of Government: The Political Economy of State and Local Public Pensions.” Journal of Public Economics 116: 89-105.

Lenney, Jamie, Byron Lutz, Finn Schüle, and Louise Sheiner. 2021. “The Sustainability of State and Local Pensions: A Public Finance Approach.” Brookings Papers on Financial Exercise (Spring): 1-48.

Lucas, Deborah J. 2017. “Towards Fair Value Accounting for Public Pensions: The Case for Delinking Disclosure and Funding Requirements.” Ready for Gathering Storm: The Dangers of State Pension Underfunding Convention (October 19-20). Cambridge, MA: Harvard Kennedy College. Citations are to an unpublished 2020 model.

Lucas, Deborah. 2021. “Comments and General Discussion of ‘The Sustainability of State and Local Pensions: A Public Finance Approach.’” Brookings Papers on Financial Exercise (Spring): 49-57.

Novy-Marx, Robert and Joshua D. Rauh. 2014. “Linking Benefits to Investment Performance in US Public Pension Systems.” Journal of Public Economics 116:47–61.

Public Plans Database. 2001-2021. Heart for Retirement Analysis at Boston School, MissionSquare Analysis Institute, Nationwide Affiliation of State Retirement Directors, and Authorities Finance Officers Affiliation.

Rauh, Joshua. 2021. “Comments and General Discussion of ‘The Sustainability of State and Local Pensions: A Public Finance Approach.’” Brookings Papers on Financial Exercise (Spring): 57-63.

Samuelson, Paul A. 1958. “An Exact Consumption-Loan Model of Interest with or without the Social Contrivance of Money.” Journal of Political Financial system 66(6): 467-482.

Sheiner, Louise. 2021. “What Debt Crisis? Time to Stop Worrying and Spend What’s Needed to Fix the Economy.” Milken Institute Assessment. Obtainable at:

Society of Actuaries. 2014. Blue Ribbon Panel on Public Pension Plan Funding. Schaumberg, IL.

S&P World Rankings. 2019. “U.S. Public Finance 2018 12 months in Assessment.” New York, NY.

U.S. Authorities Accountability Workplace (GAO). 2008. State and Local Government Retiree Benefits: Current Funded Status of Pension and Health Benefits. Washington, DC.

U.S. Social Safety Administration. 2020. The Annual Reports of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds.Washington, DC: U.S. Authorities Printing Workplace.

Appendix

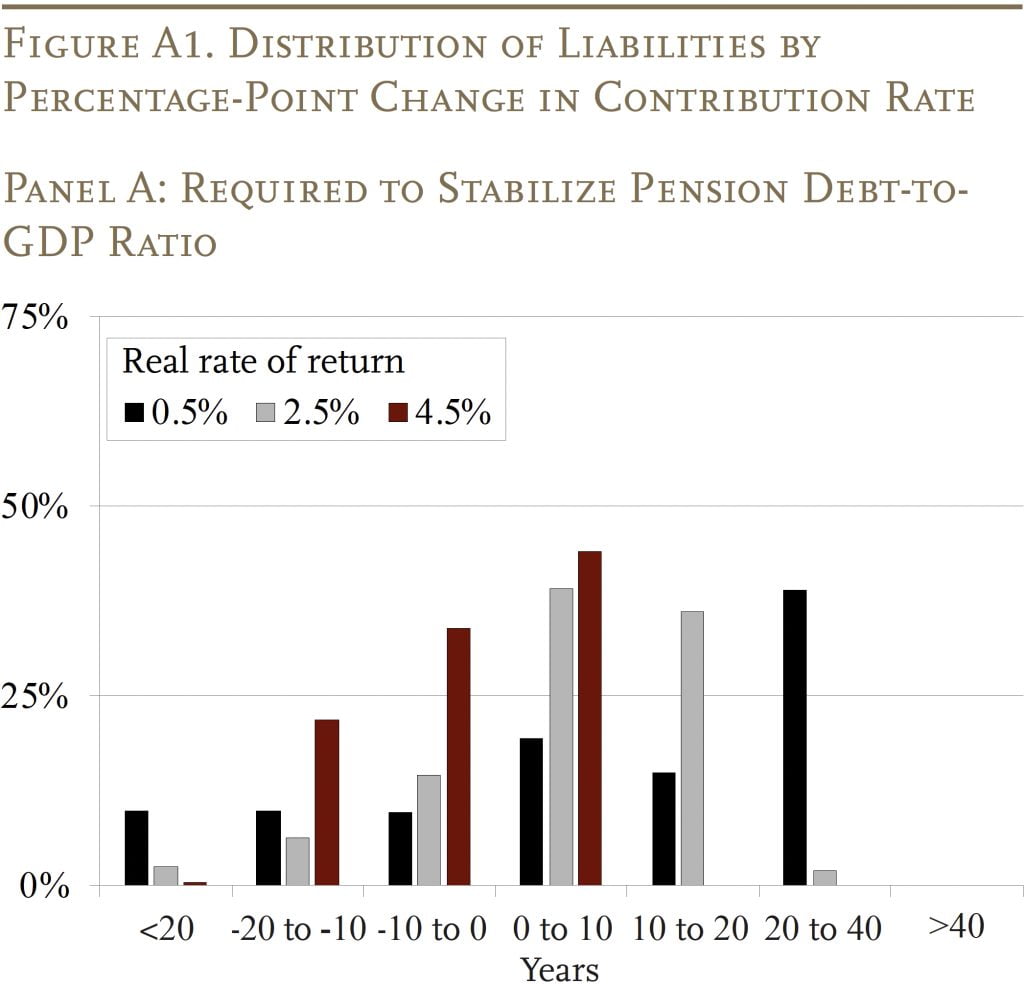

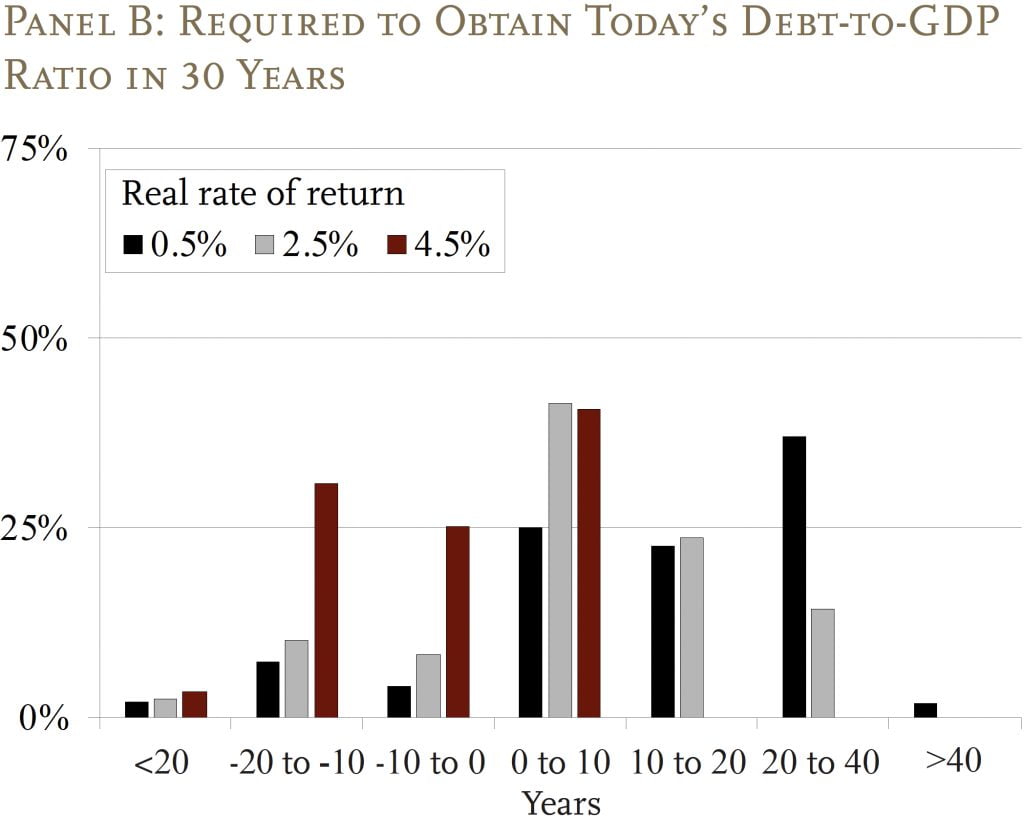

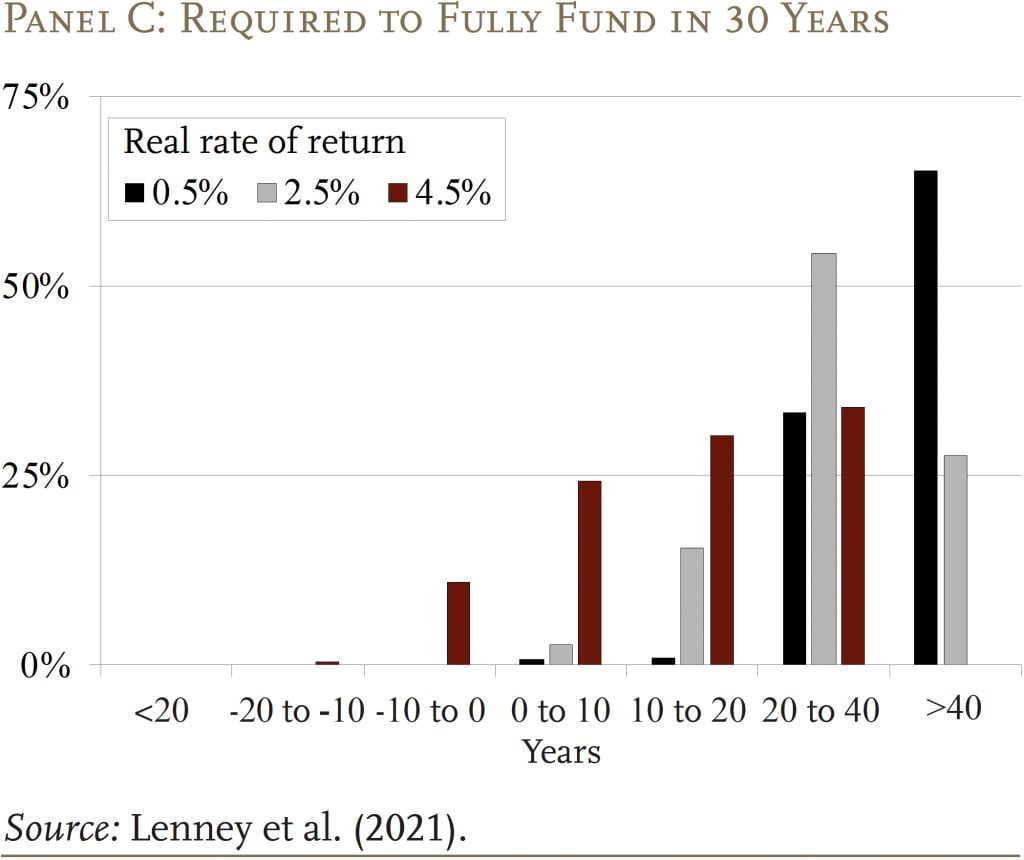

The required enhance in contribution charges to totally fund state and native plans varies considerably amongst plans. Panel A of Determine A1 exhibits the distribution of required changes for plans to stabilize the debt over the long term beginning instantly. For instance, on the 2.5-percent charge of return, solely 2 % of liabilities are in plans that want to extend funding by greater than 20 % of payroll, and fewer than 40 % of liabilities are in plans the place the contribution enhance is greater than 10 % of payroll. At a 0.5-percent return, nonetheless, 39 % want to extend contributions by greater than 20 % of payroll. Panel B exhibits the adjustments required to acquire at this time’s debt-to-GDP ratio in 30 years, and the outcomes look fairly related.

Lastly, Panel C, which presents the distribution of required contribution adjustments to totally fund the plans, exhibits a lot of the liabilities are in plans that require at the very least a 20-percentage-point enhance within the charge, and even when plans earn 4.5 % on their belongings, they should make a considerable enhance of their contribution charges.

{kind=link}