Danger-free authorities Treasury yields have risen dramatically over the previous 12 months.

The rise is a direct results of the Federal Reserve fee will increase that began in 2022.

Increased short-term yields are good for retirees and provides us a number of choices to earn risk-free returns on idle money whereas sustaining liquidity.

However the quick tempo of the Fed Funds rate of interest will increase has had unintended penalties, as we noticed final week with the failure of Silicon Valley Financial institution.

We’ve turn into so accustomed to awful authorities bond charges over the previous decade that the latest yield curve has revenue buyers sort of excited — regardless that inflation continues to be larger.

Right here’s a have a look at right this moment’s yield curve in comparison with a 12 months in the past.

Traders consider larger charges are a short-term phenomenon to take care of inflation, thereby inverting the yield curve.

That’s when short-term charges are larger than long-term charges — particularly when the 2-year fee is larger than the 10-year fee.

An inverted yield curve is indicative of a possible forthcoming recession.

However the 2-10 hole has narrowed previously week because of the anticipation the Federal Reserve could pause or gradual the tempo of future fee will increase because of the regional banking volatility.

A “regular” yield curve is indicative of a wholesome rising financial system. It slopes from backside left to proper, because the purple line depicts.

Brief-term Treasury yields now beat most high-yield savings accounts and dividend ETFs, making them a horny revenue funding.

Proudly owning Treasurys might be as simple as establishing a core place “sweep” along with your brokerage account, the place any idle money is swept into an interest-bearing account.

Traders may also purchase particular person bonds or term-specific bond funds or ETFs to realize publicity and obtain the yield.

Some buyers could even query if the time is true to promote shares to purchase authorities bonds in mild of the upper fee surroundings and market volatility.

For long-term buyers, the reply is not any.

As a basic rule, shares outperform bonds — by lots. That is very true because the funding horizon turns into longer.

So attempting to time the market by exiting shares and going into authorities bonds is a nasty concept.

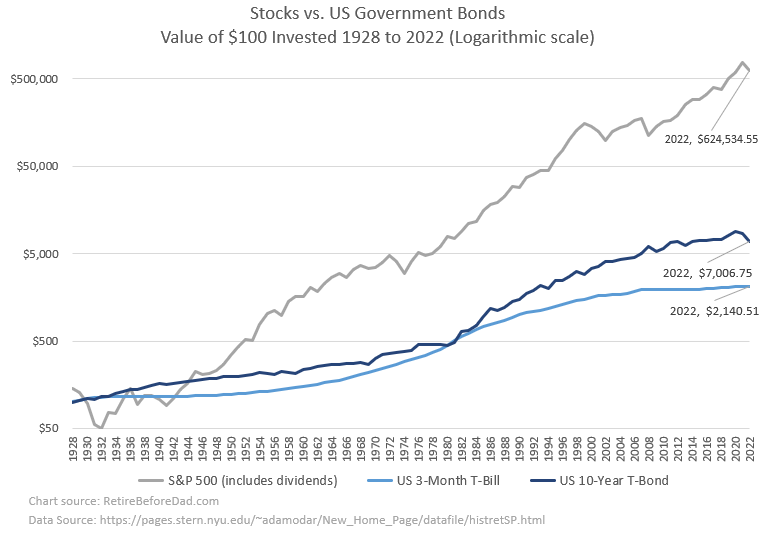

Right here’s a chart exhibiting the long-term returns of shares vs. brief and longer-term bonds because the begin of 1928:

Knowledge Supply Hyperlink: stern.nyu.edu

Knowledge Supply Hyperlink: stern.nyu.eduBetween 1928 and the tip of 2022, shares outperformed the 10-year Treasury bond by 89 occasions.

A $100 funding within the S&P 500 at first of 1928 would have been price $624,534.55 by the tip of 2022, together with dividends.

The identical $100 funding over the identical interval in 10-year T-Bonds could be price $7,006.75, and short-term 3-month T-Payments could be price $2,140.51.

So for many of us with a long-term outlook (5+ years), it solely is smart to promote shares to purchase bonds when adjusting your portfolio’s stock-to-bond ratio or throughout annual portfolio rebalancing (extra on stock-to-bond ratio at the end *).

Peter Lynch highlights one exception to the stocks-outperform-bonds rule in his 1993 ebook, Beating the Avenue.

When to Promote Shares and Purchase Bonds (Based on Peter Lynch)

Peter Lynch is the legendary mutual fund supervisor who ran Constancy’s Magellan fund from 1977 by means of 1990. The fund averaged a 29.2% annual return throughout his tenure, beating the S&P 500 by greater than double.

His books have been among the many first I learn whereas getting started investing within the mid-Nineties.

Lynch obtained his undergraduate diploma from Boston Faculty, the place an in depth buddy of mine was finding out finance and really useful his books One Up on Wall Street and Beating the Street.

I remembered a passage in one of many books about when to promote shares and purchase bonds and tracked down a replica to refresh my reminiscence.

Lynch spends most of Beating the Avenue encouraging buyers to personal shares as a substitute of bonds.

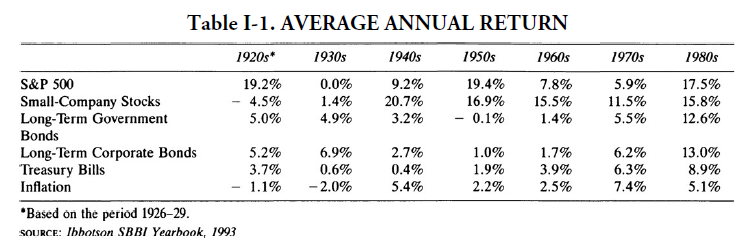

He used an identical inventory vs. bonds comparability because the chart above. His comparability was from the Twenties by means of about 1990.

Supply: Beating the Avenue

Supply: Beating the AvenuePeter’s Precept #2:

Over your complete 64 years coated within the desk, a $100,000 funding in long-term authorities bonds would now be price $1.6 million, whereas the identical quantity invested within the S&P 500 could be price $25.5 million. Gents preferring bonds don’t know what they’re lacking.

He’s constant along with his choice for shares over bonds, with one exception.

Peter’s Precept #8 — the one exception to the final rule that proudly owning shares is best than proudly owning bonds:

When yields on long-term authorities bonds exceed the dividend yield of the S&P 500 by 6 p.c or extra, promote your shares and purchase bonds.

He provides context:

Rates of interest had gone so excessive that my greatest place within the fund for a number of months working was long-term Treasury bonds. Uncle Sam was paying 13–14 p.c on these. I didn’t purchase bonds for defensive functions as a result of I used to be afraid of shares, as many buyers do. I purchased them as a result of the yields exceeded the returns one might usually anticipate to get from shares.

Rates of interest within the early Nineteen Eighties soared as Paul Volker raised the Fed Funds fee to quash inflation. Although the financial system suffered within the brief time period, Volker is taken into account a hero for making the tough choice to set off a recession to finish the Seventies-era inflation for good.

Lynch assumed the super-high charges wouldn’t final lengthy and acquired long-term U.S. bonds. It’s unclear if he held to maturity or not.

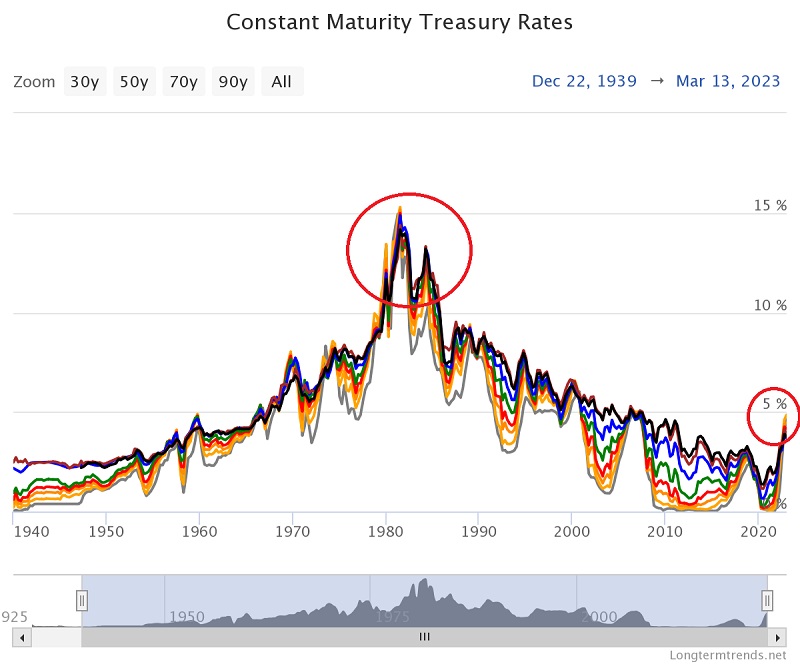

The Nineteen Eighties have been an anomaly over the previous 80 years. Charges peaked in 1980-1981. Then, from the early Nineteen Eighties till 2022, authorities bond charges trended downward.

Supply: LongtermTrends.net

Supply: LongtermTrends.netSeeing right this moment’s charges in comparison with the previous 80 years, we look like within the early phases of reversing the 40-year downward pattern. However we’re nonetheless removed from some extent the place it is smart to promote shares to purchase bonds.

The S&P 500 yield is slightly below 2%, and the 10-year T-Bond yields 3.7%.

So in accordance with Peter’s Precept #8, we’re nonetheless 4.3 proportion factors away from after we’d even start to think about promoting shares to purchase bonds.

His precept is smart as a result of if long-term inventory market returns common 9% a 12 months with important market threat, wouldn’t you settle for an 8% risk-free return?

However even then, we’re not mutual fund managers. Such excessive charges could also be a chance to place new funding {dollars} into long-term risk-free bonds, however I’d be hesitant to promote shares for that goal contemplating a number of components akin to capital achieve taxes, abandoning winners, and overthinking.

Right here’s the yield curve from August twenty first, 1981, in comparison with right this moment:

We’re nowhere close to Nineteen Eighties inflation or rate of interest ranges, but larger charges are throwing banks for a loop. That’s as a result of everybody’s turn into accustomed to low charges.

As soon as inflation begins to normalize nearer to 2%, the Federal Reserve can ease charges once more. However at this stage, we don’t know the way far they might want to elevate charges to quell inflation or if going larger will trigger different bare swimmers to be uncovered.

Will charges go as excessive because the Nineteen Eighties? Let’s hope not.

And when charges do come down once more, who is aware of how far?

Maintain onto that pre-2022 mortgage.

* Decide Your Inventory-to-Bond Portfolio Ratio

Right here’s a rule of thumb to find out your stock-to-bond portfolio ratio.

120 minus your age = % shares in your portfolio.

In case you have the next threat tolerance, use 130. Decrease, use 110.

For instance, I’m 47, and my threat tolerance is excessive. So my stock-to-bond ratio is about 83/17.

Decide your stock-to-bond ratio and stick with it no matter rates of interest or market exercise.

Favourite instruments and funding providers proper now:

Fundrise – The best strategy to spend money on high-quality actual property with as little as $10 (review)

Empower (Personal Capital is now Empower) – A free instrument to trace your internet price and analyze investments.

M1 Finance – A prime on-line dealer for long-term buyers and dividend reinvestment (review)

SaveBetter – SaveBetter is an easier strategy to entry high-yield, FDIC-insured financial savings merchandise.

{kind=link}