One of the problems that many individuals have been involved with throughout this recession is what occurs when a financial institution is seized by the FDIC. It is a matter of concern as a result of the recession noticed fairly a couple of financial institution closings, and there are nonetheless a whole lot of banks nonetheless on the FDIC watch record for potential failures.

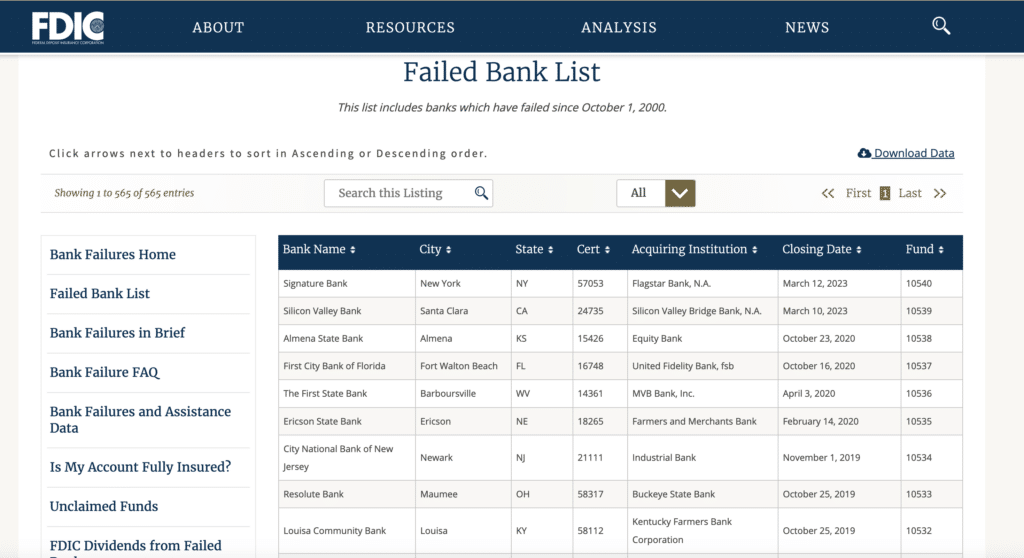

As of the March of this 12 months in accordance with the FDIC, there have been 565 financial institution closings since Oct 1st, 2000. Whereas the worst is presumed to be over, you by no means know when your financial institution may very well be taken over by the FDIC.

Fast Observe:

You possibly can see the variety of financial institution closings on the FDIC website beneath their list of Failed Banks.

The FDIC Closes a Financial institution

When the FDIC decides to shut a financial institution, it tries to maintain issues quiet up till the final minute. That is to stop a run on the financial institution, ought to customers get wind of the upcoming motion. When they’re prepared, the parents from the FDIC head into the financial institution and shut down operations. This virtually all the time takes place on a Friday. The FDIC tries to shut down all branches of the financial institution directly, when doable. The financial institution is closed over the weekend.

The FDIC tries very arduous to have one other financial institution lined as much as take over the failed financial institution. If this doesn’t occur, then financial institution is positioned beneath FDIC conservatorship, and the FDIC runs the financial institution. This takes time and sources, although, so, when doable, the FDIC likes another financial institution to take over.

Whether or not or not the FDIC has somebody lined up, many banks are opened to the general public the next Monday. FDIC folks spend the weekend with financial institution workers, managers and house owners, determining the state of the financial institution, organizing belongings and liabilities.

Different businesses can become involved to assist out, such because the Workplace of Comptroller of the Forex (to cope with bank cards), the Workplace of Thrift Supervision, and even state businesses. When the financial institution is reopened on Monday, prospects can proceed enterprise as standard.

What Occurs to Your Cash

When the FDIC seizes a financial institution, your cash is often protected. The FDIC insures deposit accounts for as much as $250,000 per depositor per financial institution (this quantity has been made everlasting), so if the financial institution fails, you may nonetheless get your cash. If another person has taken over the financial institution, then your accounts often switch to that financial institution, and you’ll determine whether or not or to not go away them there.

If the FDIC has conservatorship of the financial institution, there’s a good probability that it’ll merely start slicing checks to customers and making an attempt to promote different belongings.

In case your financial institution is closed by the FDIC, and no different financial institution takes over, you’re going to get your cash. You’ll have to face in line for hours, or wait a few weeks to get your test. If the financial institution is closed, uncleared transactions could also be returned.

You possibly can have charges refunded, however there may be quite a lot of trouble concerned, and you have to to guarantee that your entire computerized debit transactions are up to date (you could want to do that even when one other financial institution takes over).

Moreover, because you don’t have entry to your cash when you wait on your test, you may lose out on curiosity that you just may need earned on some deposit accounts. A brand new financial institution could require that you just get a brand new CD (at a presumably decrease price), or alter a few of your different deposits and accounts.

| Step Quantity | Description | Affect on Clients |

|---|---|---|

| 1 | FDIC identifies a wholesome financial institution to amass the failed financial institution (if doable) | – Accounts transferred to buying financial institution – Continued entry to funds – Notification of modifications to account phrases and situations |

| 2 | FDIC liquidates the failed financial institution (if no buying financial institution is discovered) | – Insured deposits paid out as much as the protection restrict – Doable receipt of a test, an account at one other insured financial institution, or one other type of fee |

| 3 | Dealing with of loans and different banking companies | – Switch of loans and companies to buying financial institution (if financial institution is acquired) – Notification of modifications to mortgage phrases or fee info (if financial institution is liquidated and loans are offered to different banks) |

| 4 | Communication with prospects | – FDIC communicates by the financial institution’s web site, native information, and mailed notices – Clients should hold contact info updated to obtain vital updates |

| 5 | Entry to insured deposits | – Clients can sometimes entry their insured deposits inside a couple of days of the financial institution’s closure |

| 6 | Restoration of uninsured funds (if relevant) | – Doable restoration of some or all uninsured funds, relying on the proceeds from the financial institution’s liquidation – No assure of full restoration of uninsured funds |

| 7 | Decision of the failed financial institution | – General decision course of can take months and even years, relying on the complexity of the financial institution’s belongings and liabilities |

Debt Does Not Go Away

As you may think, your debt stays intact as nicely. It’s both administered by the brand new financial institution that has taken over, or it’s offered to a different lender. Any loans you’ve got with the failed financial institution will seem on the stability sheet, and be taken care of.

Investments made by the financial institution could be one other story, although. Since these usually are not FDIC insured, you may maintain losses. You’ll have to double test.

Backside line – Your Financial institution Account and the FDIC

Your money deposits, so long as you don’t exceed $250,000 insured. Nevertheless, there are different prices, together with these of time and comfort, related to the FDIC seizure of a financial institution. You possibly can put together for such an eventuality by checking up on the health of your bank, and having a again up plan, simply in case you’ve got restricted entry to your cash for a time.

FAQs – Financial institution Fails and FDIC Safety

When a financial institution is seized by the FDIC, it signifies that the financial institution has failed, and the FDIC steps in to handle the state of affairs. The FDIC will both discover a wholesome financial institution to amass the failed financial institution’s belongings and liabilities or liquidate the financial institution and pay out insured deposits.

Sure, your cash is protected as much as the insured restrict. The FDIC insures deposits at member banks as much as $250,000 per depositor, per insured financial institution, for every account possession class. This consists of checking accounts, financial savings accounts, cash market deposit accounts, and certificates of deposit (CDs).

The FDIC works shortly to resolve failed banks. Most often, prospects can entry their insured deposits inside a couple of days of the financial institution’s closure.

Nevertheless, the general decision course of can take months and even years, relying on the complexity of the failed financial institution’s belongings and liabilities.

You possibly can test in case your financial institution is FDIC-insured by searching for the FDIC brand at your financial institution department, on the financial institution’s web site, or in your account statements. You may also use the FDIC’s BankFind software (https://research2.fdic.gov/bankfind/) to confirm your financial institution’s insurance coverage standing.

One of the problems that many individuals have been involved with throughout this recession is what occurs when a financial institution is seized by the FDIC. It is a matter of concern as a result of the recession noticed fairly a couple of financial institution closings, and there are nonetheless a whole lot of banks nonetheless on the FDIC watch record for potential failures.

As of the March of this 12 months in accordance with the FDIC, there have been 565 financial institution closings since Oct 1st, 2000. Whereas the worst is presumed to be over, you by no means know when your financial institution may very well be taken over by the FDIC.

Fast Observe:

You possibly can see the variety of financial institution closings on the FDIC website beneath their list of Failed Banks.

The FDIC Closes a Financial institution

When the FDIC decides to shut a financial institution, it tries to maintain issues quiet up till the final minute. That is to stop a run on the financial institution, ought to customers get wind of the upcoming motion. When they’re prepared, the parents from the FDIC head into the financial institution and shut down operations. This virtually all the time takes place on a Friday. The FDIC tries to shut down all branches of the financial institution directly, when doable. The financial institution is closed over the weekend.

The FDIC tries very arduous to have one other financial institution lined as much as take over the failed financial institution. If this doesn’t occur, then financial institution is positioned beneath FDIC conservatorship, and the FDIC runs the financial institution. This takes time and sources, although, so, when doable, the FDIC likes another financial institution to take over.

Whether or not or not the FDIC has somebody lined up, many banks are opened to the general public the next Monday. FDIC folks spend the weekend with financial institution workers, managers and house owners, determining the state of the financial institution, organizing belongings and liabilities.

Different businesses can become involved to assist out, such because the Workplace of Comptroller of the Forex (to cope with bank cards), the Workplace of Thrift Supervision, and even state businesses. When the financial institution is reopened on Monday, prospects can proceed enterprise as standard.

What Occurs to Your Cash

When the FDIC seizes a financial institution, your cash is often protected. The FDIC insures deposit accounts for as much as $250,000 per depositor per financial institution (this quantity has been made everlasting), so if the financial institution fails, you may nonetheless get your cash. If another person has taken over the financial institution, then your accounts often switch to that financial institution, and you’ll determine whether or not or to not go away them there.

If the FDIC has conservatorship of the financial institution, there’s a good probability that it’ll merely start slicing checks to customers and making an attempt to promote different belongings.

In case your financial institution is closed by the FDIC, and no different financial institution takes over, you’re going to get your cash. You’ll have to face in line for hours, or wait a few weeks to get your test. If the financial institution is closed, uncleared transactions could also be returned.

You possibly can have charges refunded, however there may be quite a lot of trouble concerned, and you have to to guarantee that your entire computerized debit transactions are up to date (you could want to do that even when one other financial institution takes over).

Moreover, because you don’t have entry to your cash when you wait on your test, you may lose out on curiosity that you just may need earned on some deposit accounts. A brand new financial institution could require that you just get a brand new CD (at a presumably decrease price), or alter a few of your different deposits and accounts.

| Step Quantity | Description | Affect on Clients |

|---|---|---|

| 1 | FDIC identifies a wholesome financial institution to amass the failed financial institution (if doable) | – Accounts transferred to buying financial institution – Continued entry to funds – Notification of modifications to account phrases and situations |

| 2 | FDIC liquidates the failed financial institution (if no buying financial institution is discovered) | – Insured deposits paid out as much as the protection restrict – Doable receipt of a test, an account at one other insured financial institution, or one other type of fee |

| 3 | Dealing with of loans and different banking companies | – Switch of loans and companies to buying financial institution (if financial institution is acquired) – Notification of modifications to mortgage phrases or fee info (if financial institution is liquidated and loans are offered to different banks) |

| 4 | Communication with prospects | – FDIC communicates by the financial institution’s web site, native information, and mailed notices – Clients should hold contact info updated to obtain vital updates |

| 5 | Entry to insured deposits | – Clients can sometimes entry their insured deposits inside a couple of days of the financial institution’s closure |

| 6 | Restoration of uninsured funds (if relevant) | – Doable restoration of some or all uninsured funds, relying on the proceeds from the financial institution’s liquidation – No assure of full restoration of uninsured funds |

| 7 | Decision of the failed financial institution | – General decision course of can take months and even years, relying on the complexity of the financial institution’s belongings and liabilities |

Debt Does Not Go Away

As you may think, your debt stays intact as nicely. It’s both administered by the brand new financial institution that has taken over, or it’s offered to a different lender. Any loans you’ve got with the failed financial institution will seem on the stability sheet, and be taken care of.

Investments made by the financial institution could be one other story, although. Since these usually are not FDIC insured, you may maintain losses. You’ll have to double test.

Backside line – Your Financial institution Account and the FDIC

Your money deposits, so long as you don’t exceed $250,000 insured. Nevertheless, there are different prices, together with these of time and comfort, related to the FDIC seizure of a financial institution. You possibly can put together for such an eventuality by checking up on the health of your bank, and having a again up plan, simply in case you’ve got restricted entry to your cash for a time.

FAQs – Financial institution Fails and FDIC Safety

When a financial institution is seized by the FDIC, it signifies that the financial institution has failed, and the FDIC steps in to handle the state of affairs. The FDIC will both discover a wholesome financial institution to amass the failed financial institution’s belongings and liabilities or liquidate the financial institution and pay out insured deposits.

Sure, your cash is protected as much as the insured restrict. The FDIC insures deposits at member banks as much as $250,000 per depositor, per insured financial institution, for every account possession class. This consists of checking accounts, financial savings accounts, cash market deposit accounts, and certificates of deposit (CDs).

The FDIC works shortly to resolve failed banks. Most often, prospects can entry their insured deposits inside a couple of days of the financial institution’s closure.

Nevertheless, the general decision course of can take months and even years, relying on the complexity of the failed financial institution’s belongings and liabilities.

You possibly can test in case your financial institution is FDIC-insured by searching for the FDIC brand at your financial institution department, on the financial institution’s web site, or in your account statements. You may also use the FDIC’s BankFind software (https://research2.fdic.gov/bankfind/) to confirm your financial institution’s insurance coverage standing.

{kind=link}