They’d enhance transparency and most certainly returns by investing in index funds.

I need to admit, I adore it when analysis helps my intestine. Therefore, I’m delighted to report the findings from the new study by my colleagues JP Aubry and Yimeng Yin that compares precise returns earned by state and native pension plans with returns from a easy index portfolio of 60 % US shares (Russell 3000 Whole Return Index) and 40 % US bonds (Bloomberg US Mixture Bond Index), with a 10-basis level administration payment.

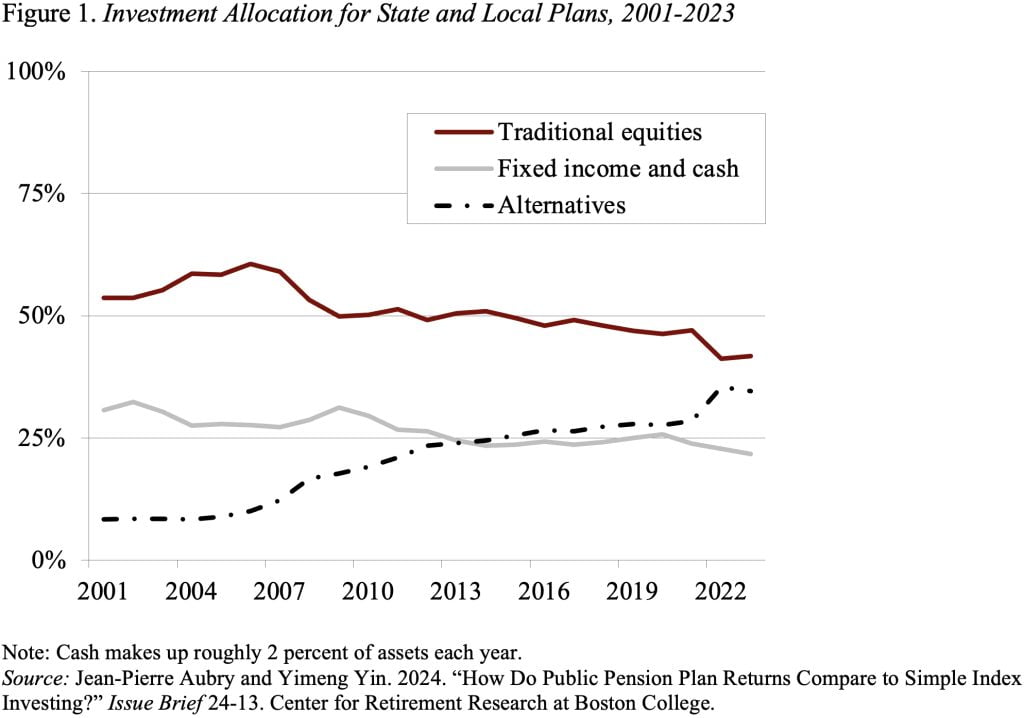

The efficiency difficulty has arisen as a result of state and native plans have been shifting their portfolios from conventional equities and bonds to different belongings, equivalent to personal equities, hedge funds, actual property, and commodities (see Determine 1).

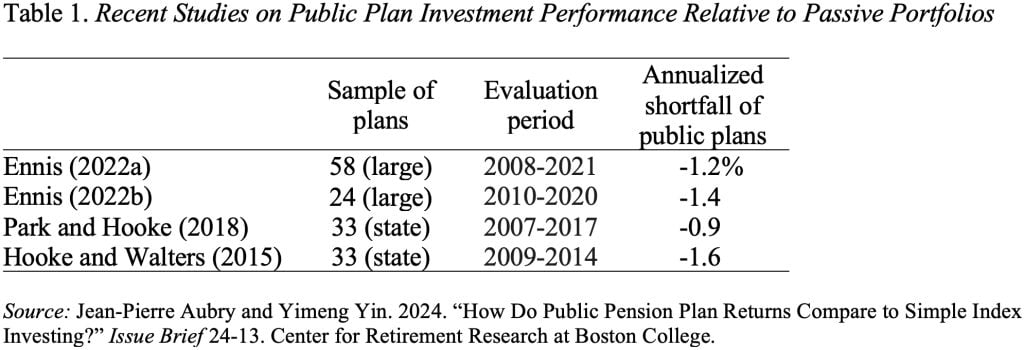

JP and Yimeng should not the primary researchers to match precise returns for state and native plans to a easy listed method. Plenty of current research have proven that public plans in combination underperform index portfolios by 0.9 % to 1.6 % annualized (see Desk 1).

Critics counter that the findings so far, nevertheless, rely closely on the time interval analyzed. Additional complicating the dialogue is pension funds’ use of lagged returns for some different belongings, which might distort their general reported return.

To handle these considerations, JP and Yimeng examine precise returns to the 60/40 method over varied time intervals, utilizing pension returns adjusted for lagged reporting.

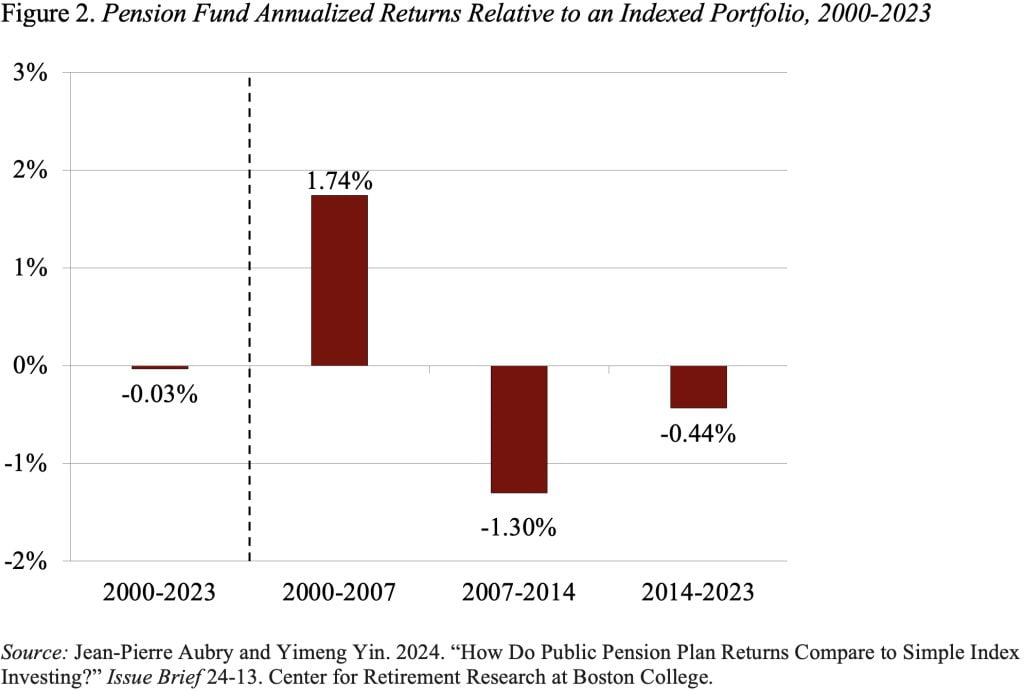

The primary takeaway from their new research is that, as proven in Determine 2, the long-term annualized return for pension funds is nearly the identical as that of the 60/40 portfolio (about 6.1 % for each).

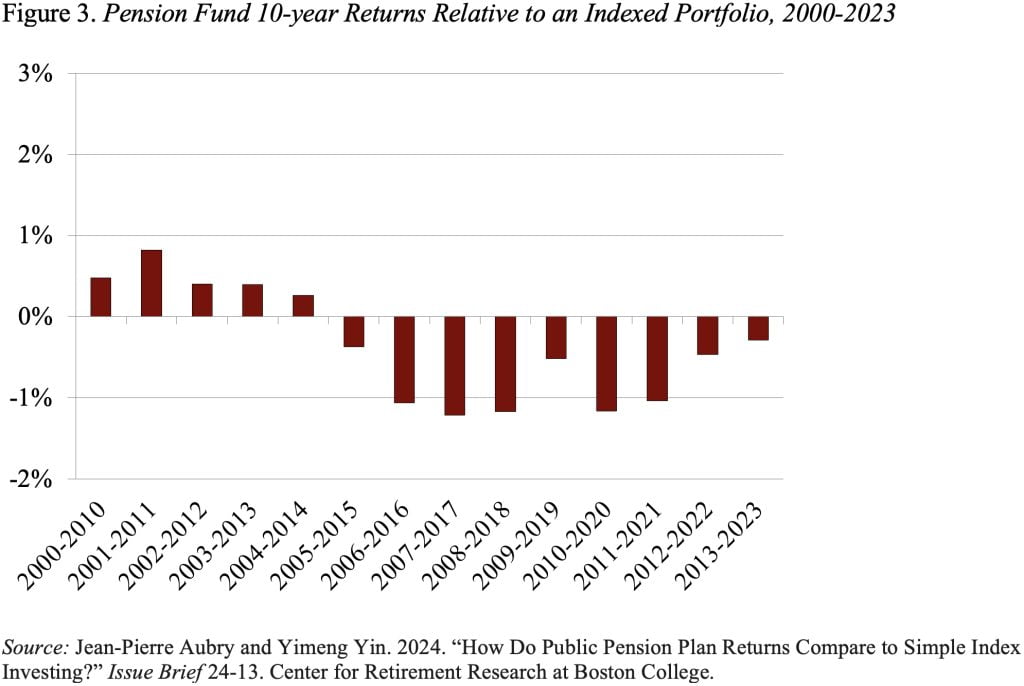

Nevertheless, the outcomes additionally reveal an attention-grabbing two-part story underlying this comparable efficiency – state and native plans did a lot better than the index funds earlier than the International Monetary Disaster and far worse post-crisis. This sample additionally reveals up in Determine 3, which compares efficiency over every 10-year interval between 2000 to 2023.

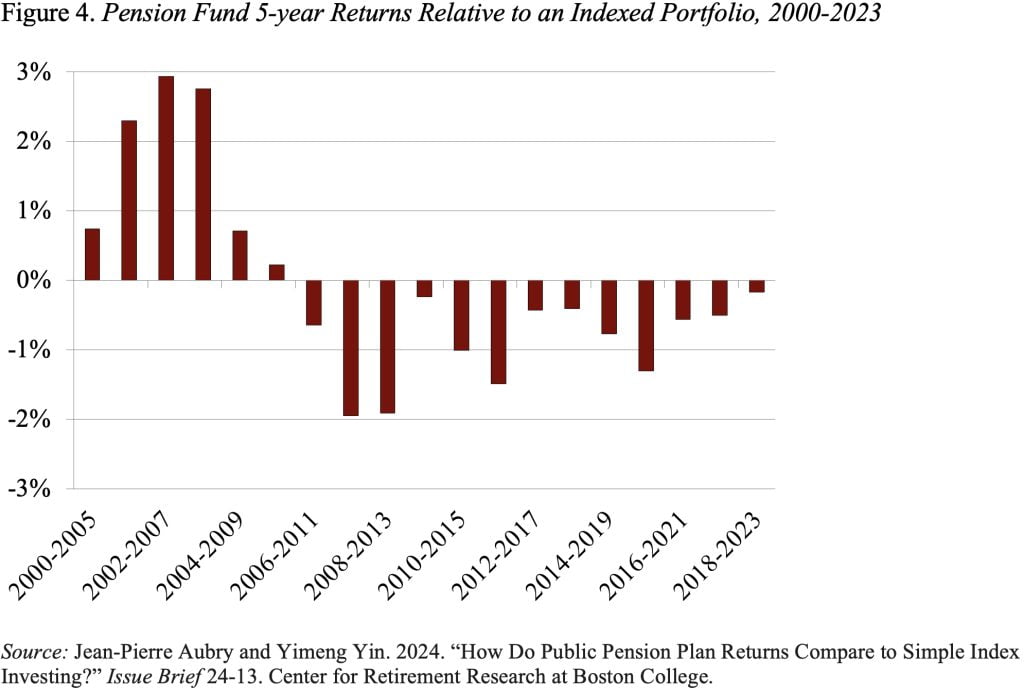

Lastly, the authors offered outcomes for every 5-year interval between 2000 and 2023. Once more, the general outcomes are comparable (see Determine 4). State and native plans did higher by 2010 and have fallen brief every interval afterward.

The clear message from this analysis is that state and native plans can not moderately anticipate extraordinary long-term returns from an opaque technique involving advanced belongings and lively administration. In such a world, public plans ought to most likely follow a clear method of easy index funds.

{kind=link}