WHAT IS OCCAM’S RAZOR? Occam’s Razor is a precept attributed to William Occam, a 14th century thinker. He harassed that explanations should not be multiplied past what is critical. Thus, Occam’s Razor is a time period used to “shave off” or dismiss superfluous explanations for a given occasion. This idea is essentially ignored throughout the funding administration panorama. This text will “shave off ” widespread funding misinformation and current what’s necessary for attaining long-term funding success.

Investing entails threat. Whenever you put your cash to work within the monetary markets there’s all the time an opportunity, over each time interval, that you possibly can lose cash. More often than not, particularly over longer time frames, the market goes up. However they don’t should. The chance is all the time there – and that risk is what investing is about.

However there are issues that you are able to do to regulate the chance that you’re dealing with (past your asset allocation) And one of many less complicated issues you are able to do is to make use of Buffer Property when you’re taking cash out of your portfolio.

What are Buffer Property?

Buffer belongings are precisely what they sound like. They’re very low threat belongings which can be largely uncorrelated along with your funding portfolio that function a buffer between the vicissitudes of the market and your spending. Some typical examples of buffer belongings are issues like a line of credit from a reverse mortgage, the money worth of a complete life insurance coverage coverage, or simply plain money. Primarily, buffer belongings assist you to management when it’s essential to promote unstable (and better returning) belongings out of your portfolio to fund your spending. They’re there to help manage your sequence of returns risk.

Within the “excellent” world of an intro to investing class, the sequence of your returns doesn’t matter. As long as you aren’t placing any cash into, or taking cash out of your portfolio, it doesn’t matter how the returns you expertise are organized – all of it simply goes into the portfolio’s whole return equally. However that first half, that no cash goes into or out of your portfolio, doesn’t normally maintain. For many of us, we’re both actively saving cash into our funding portfolio whereas we’re working (hopefully), or we’re spending out of that portfolio after we’re retired. After we add these cashflows into the combination, the order that we expertise returns issues.

Usually, that is the place we begin taking about how your sequence of returns threat is highest proper round retirement (or extra particularly while you begin taking distributions out of your portfolio). That’s usually the purpose when your portfolio is the biggest, and you might be locking in any losses (or beneficial properties) while you take cash out. And that is completely true.

However I wish to spotlight an necessary corollary – in retirement your sequence of returns threat is all the time reducing. This 12 months’s returns may have a higher impression on the probability that you just’ll have the ability to meet your deliberate spending all through your life, than another 12 months sooner or later. In different phrases, this 12 months’s return is all the time a very powerful one.

Ideally, we’d wish to keep away from promoting when the market is down to reduce our sequence of returns threat. That is the place buffer belongings may also help.

How Buffer Property Can Assist Handle Sequence of Returns Danger

Buffer belongings may also help mitigate sequence of returns threat by separating your spending from when it’s essential to promote belongings out of your funding portfolio – no less than to a degree. There are two foremost approaches for the way to do that.

The primary strategy is to deal with your buffer belongings as basically reserves. With this strategy, you retain a giant pool of cash off to the facet you could spend from within the years when your portfolio is down (or beneath some particular return). This strategy is fairly easy, but it surely does require lots of belongings to be held in reserve on the entrance finish.

The second strategy is to make use of your buffer belongings extra as working capital. You’ve got a (smaller) pool of cash that you just do all your spending from – whether or not the market is having an excellent 12 months or not – and also you refill that pool each time it’s advantageous.

So, as an example, say that I’m utilizing this strategy and I’ve sufficient buffer belongings to cowl three years of spending. Throughout the first 12 months, I’ll take my distributions from my buffer belongings, after which on the finish of the 12 months I’ll look to see how my portfolio carried out. If the markets cooperated, I’ll promote sufficient dangerous belongings to carry my buffer belongings again as much as 3 years of spending. But when the markets had a foul 12 months, I wouldn’t do something. Subsequent 12 months I’ll proceed to eat into my buffer. Then on the finish of the 12 months, I’ll have a look at my returns once more and see if the market has recovered. If it has, I can begin constructing again up my buffer. You’re basically constructing a runway on your spending.

Whereas buffer belongings are an excellent instrument for managing your sequence threat, there’s all the time a tradeoff. Holding buffer belongings means that you’re holding a reimbursement out of your funding portfolio. It’s good to take into account whether or not lowering your publicity to sequence threat is value lowering the potential upside out of your funding portfolio.

How Large of a Buffer Do You Want?

If you happen to do resolve to make use of buffer belongings, it’s essential to take into consideration how large of a buffer you want. The larger your buffer – the longer you possibly can go with out promoting out of your funding portfolio – the extra you defend your self towards sequence of returns threat – however the extra potential development you surrender.

A method to determine how large of a buffer chances are you’ll wish to use is to have a look at the historic information.

If you’re desirous about the primary strategy to buffer belongings that we mentioned – conserving a giant pile of cash on the facet to spend via when the market is down – you’ll wish to be desirous about what number of years the market shall be down throughout your retirement. If you’re going with the second strategy – conserving a smaller buffer that you just spend from and replenish, you’ll wish to be desirous about how lengthy downturns usually final.

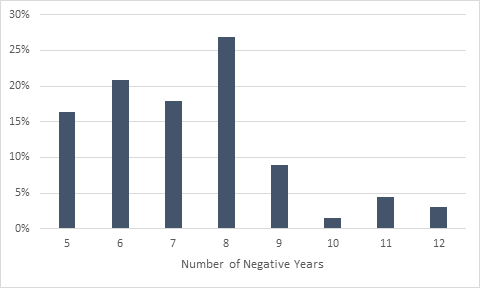

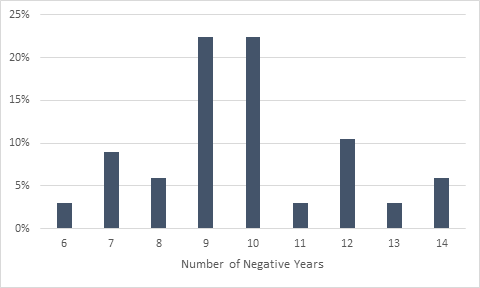

So let’s begin with the primary query: throughout a “typical” retirement, how usually will the markets lose cash over the course of a 12 months? To maintain our evaluation easy (and basically the worst case), let’s have a look at the annual returns of the S&P 500 Index from 1926 via 2021. What we wish to know is, stepping via annually, what number of years has the S&P 500 Index gone down over both a 30 or 40 12 months retirement? The extra years with a unfavourable return, the extra years you’ll be tapping your buffer belongings, and the larger buffer you’ll want.

So what are the numbers? Let’s begin with the abstract.

| 30 12 months Retirement | 40 12 months Retirement | |

| Common variety of unfavourable years | 7.3 years | 9.8 years |

| Customary Deviation | 1.7 years | 2.0 years |

| Most variety of unfavourable years | 12 years | 14 years |

| Minimal variety of unfavourable years | 5 years | 6 years |

For each lengths of retirement, we see that the S&P 500 has been down rather less than 1 / 4 of the time, although the correct (dangerous) tail does get somewhat bit ugly. However let’s have a look at the frequency of the outcomes as effectively.

Variety of Adverse Years over a 30 12 months Retirement

Variety of Adverse Years over a 40 12 months Retirement

A lot of the outcomes, for each retirement lengths, are proper across the averages (as you’ll anticipate), however there are positively some dangerous outcomes. It’s value mentioning that a lot of the actually dangerous outcomes middle across the Nice Melancholy. Utilizing the 30 12 months retirement, nobody retiring after 1931 had greater than 9 unfavourable years, and nobody retiring after 1952 had greater than 8 unfavourable years over the course of their retirement.

I’m all the time cautious of discounting information from the Nice Melancholy – it occurred – however as we take into consideration what’s prone to occur sooner or later, it’s necessary to contemplate how seemingly we’re to see a state of affairs like that once more. It might probably positively occur, however the monetary markets (and the world) are a really totally different place than they had been a century in the past.

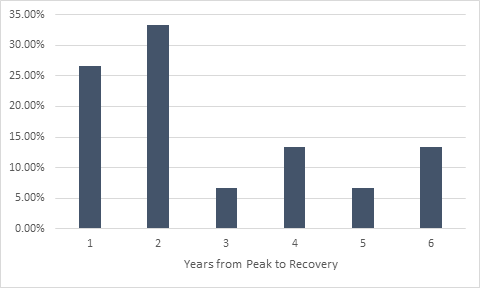

Let’s take up the case the place you spend out of your buffer belongings after which refill them when you possibly can keep away from promoting issues at a loss. With this strategy we don’t care (as a lot) about how usually the market declines, as an alternative we care about how lengthy the market takes to get again to it’s preliminary peak (encompassing each the decline and restoration).

This time round we’ll proceed trying on the S&P 500 Index, however we’ll be utilizing month-to-month information to get somewhat extra specificity. We’ll wish to give attention to durations the place the markets noticed an inexpensive decline, so we’re in search of a drop of 10% or extra from peak to trough.

Over the interval we’re , there have been 15 durations that met our standards. And so they cowl an entire lot of floor and totally different conditions. Going again to the instance we used earlier than, the Nice Melancholy took 185 months (15 years and 5 months) to get again to it’s peak in September 1929. Alternatively, in the beginning of the pandemic the market declined and rebounded again to it’s preliminary excessive in solely 7 months.

On common, it took somewhat greater than 37 months for the market to drop after which recuperate to it’s preliminary degree. Although in case you exclude the Nice Melancholy, it solely took 26.5 months on common. My earlier remark concerning the applicability of knowledge from the Nice Melancholy nonetheless stands, however it’s the clear outlier right here at 185 months from peak to restoration. The Tech Crash, which was the following longest interval, “solely” took 74 months from peak to restoration.

Total, most downturns are comparatively brief. 60% of downturns recuperate in two years or much less, and two thirds recovered by the top of 12 months 3.

How Large of a Buffer Do You Need?

Whereas taking part in with the numbers is enjoyable, we wish to use what’s occurred prior to now to tell what we are going to do going ahead. You most likely don’t wish to (and aren’t capable of) stash away 15 years of spending in your buffer belongings. So the query turns into how large of a buffer you do wish to construct into your plan (if any in any respect)? How lengthy of a runway do you wish to have the place you possibly can ignore regardless of the markets are doing?

Like most planning questions, there isn’t any proper reply. It comes right down to what you wish to do. It’s good to resolve on the dimensions that you just really feel snug with – balancing the advantage of lowering your sequence of returns threat towards the price of lowering the potential upside of your funding portfolio’s development.

Buffer belongings is usually a useful gizmo, and there may be proof that they will enhance general outcomes in the correct conditions, however they aren’t a panacea. They aren’t essentially for everybody. It all the time comes right down to what is sensible to you – what are the tradeoffs that you just wish to make in your retirement earnings plan?

{kind=link}