Everybody all the time talks about investing (and planning) for the long run. However they’re often obscure about what the “long run” really means. Does that imply 5 years? 10 years? Extra? (Spoiler: the reply is undoubtedly extra). And admittedly, speaking about how it’s essential deal with the long run can really feel like a little bit of a dodge when the markets haven’t been cooperating.

Let’s dig in and take into consideration what “long run” really means – each in idea and observe.

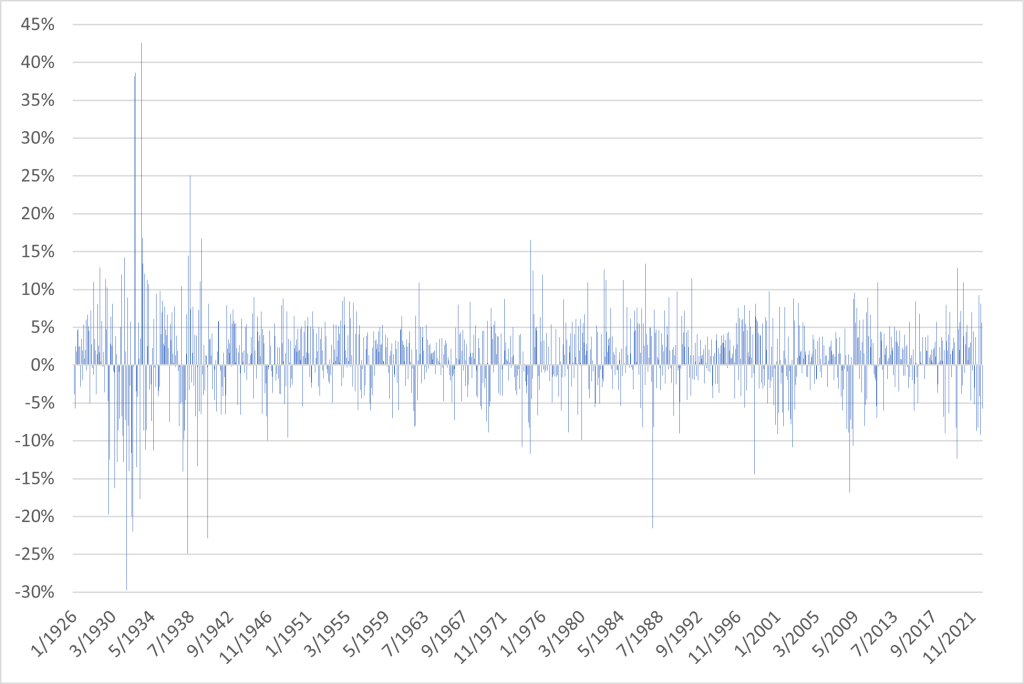

First, let’s focus on idea. Why does investing for the long run matter? It’s not just like the market retains rating and can toss us a few good years if now we have had a run of unhealthy years, or will preserve us trustworthy by throwing a nasty 12 months right into a bull run. The market is manner too messy for that. Monetary returns are practically random. A great way to see that is to only have a look at the returns. As an example, beneath, now we have the month-to-month returns of the S&P 500 Index from January 1926 to December 2022. We are able to do all types of statistical evaluation on these returns (and now we have), however it involves the identical place as simply eyeballing the information – every return is essentially random. It’s successfully unimaginable to foretell what is going to occur subsequent.

A typical manner of describing that is to say that the market strikes in a Random Stroll. Every particular person step that the market takes (the following return) is mainly random.

However not utterly random.

Whereas we might not have the ability to predict every particular person step, there’s a path that this stroll is mostly going (and we wouldn’t hassle investing if this wasn’t the case). However it’s extremely exhausting to establish this pattern over shorter time intervals. In truth, I’ve written an article about how one can’t inform brief time period inventory returns from the flip of a coin.

In essence, the “long run” is nonetheless lengthy it takes for these developments within the Random Stroll to claim themselves.

These developments are the entire completely different danger premia on provide out there. As an example, shares are riskier than bonds, so they have a tendency to have greater returns than bonds. If this weren’t true nobody would purchase shares. There’d be no purpose to. Why would you purchase one thing dangerous (shares) should you might get the identical return with a safer asset (bonds)?

These danger premia are the market’s manner of getting you to purchase dangerous property. And the riskier an asset is (no less than for certain types of risk), the larger the chance premium, and the stronger the pattern within the Random Stroll.

However it’s known as a danger premium for a purpose. It’s dangerous. There aren’t any ensures. There are completely going to be intervals – even comparatively lengthy intervals – when the Random Stroll isn’t our good friend and the randomness overwhelms the pattern.

For danger to truly be dangerous, it might’t all the time work out.

That mentioned, the longer you stick round, the extra seemingly it’s that that pattern will assert itself. However you’ll by no means get to 100% certainty – there’s all the time an opportunity that issues received’t work out irrespective of how lengthy you keep invested. That is a part of the discount we make once we put money into dangerous property. To get the upper returns “promised” by the markets, we have to settle for the chance.

However that is all very summary. It’s necessary to consider (and make peace with) however it doesn’t actually assist us put numbers round our major questions – how lengthy is the long run?

So let’s try this.

However earlier than we do, let’s take into consideration what we’re searching for. Identical to most huge elementary questions, there aren’t any definitive solutions, and no shiny traces. We’re not going to have the ability to say that 24 years is “long run,” however 23 years isn’t. We’re coping with gradations right here – completely different ranges of confidence. However placing numbers round this can assist make the query extra concrete.

As I mentioned, there are by no means any ensures with investing (I’m going to beat this level into the bottom) however we are able to see the results of an extended time horizon very clearly within the knowledge. To do that, we’ll preserve issues easy, and simply deal with the S&P 500 Index. However these similar ideas apply in all places within the monetary markets. It is a story concerning the elementary relationship between danger and return – and what meaning.

For this evaluation we’re going to be taking a look at rolling annualized returns of the S&P 500 Index over differing lengths of time from January 1926 via December 2022. What we’re asking is should you invested at a random time limit throughout this era, what would your return have been?

A very good place to begin is by trying on the vary of returns. What have been the perfect and worst returns for every holding interval? Let’s begin by trying on the knowledge.

| Holding Interval | Greatest Return | Worst Return | Complete Vary |

| 1 Yr | 162.88% | -67.57% | 230.44% |

| 3 Yr | 43.35% | -42.35% | 85.70% |

| 5 Yr | 36.12% | -17.36% | 53.48% |

| 10 Yr | 21.43% | -4.95% | 26.38% |

| 15 Yr | 19.69% | -0.41% | 20.10% |

| 20 Yr | 18.26% | 1.89% | 16.37% |

| 30 Yr | 14.78% | 7.80% | 6.98% |

| 60 Yr | 13.32% | 9.03% | 4.28% |

The outcomes listed below are pretty apparent. The longer that you’re invested, the narrower the unfold is between the extremes. However there are literally two issues happening right here which can be value speaking about. The primary is what we need to deal with – the results of your time horizon in your funding returns.

However the second is rather less apparent. We’ve fewer impartial observations with the longer time intervals. As an example, with the 1 12 months observations, now we have practically 100 separate 1 12 months intervals (annually from 1926 – 2022), however we solely have about one and a half impartial 60 12 months intervals. Which means the longer time intervals will naturally have extra overlapping knowledge. This may have a tendency to scale back the variance of the returns for these longer time intervals relative to the shorter intervals which have comparatively much less overlap within the knowledge. I don’t need to overemphasize the purpose, however it’s a limitation that we have to contemplate as we glance via all the pieces.

However even with this in thoughts, the distinction between the vary of the 1 12 months returns with the long term returns is astounding. The vary between the perfect and worst 1 12 months returns was 230%. The vary for the 60 12 months returns was solely 4.3%. And never solely that, the worst 1 12 months return instantly preceded the perfect 1 12 months return. Brief time intervals will whip your portfolio round, and actually emphasize simply how random the Random Stroll could be.

And with the long term returns, they include the entire craziness of the shorter intervals. However over time issues have balanced out. The pattern within the Random Stroll has time to indicate itself.

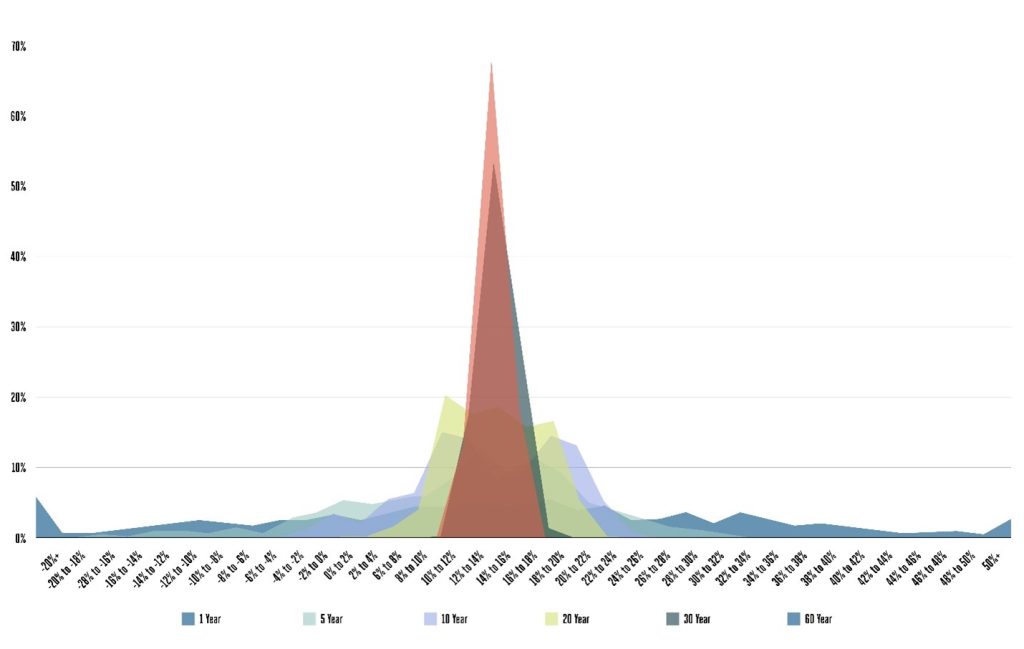

That is fascinating, however it’s purely targeted on the perimeters of the distributions. And we don’t need to do our planning primarily based on outliers. So let’s have a look at the precise distribution of returns – how typically every holding interval had a selected return.

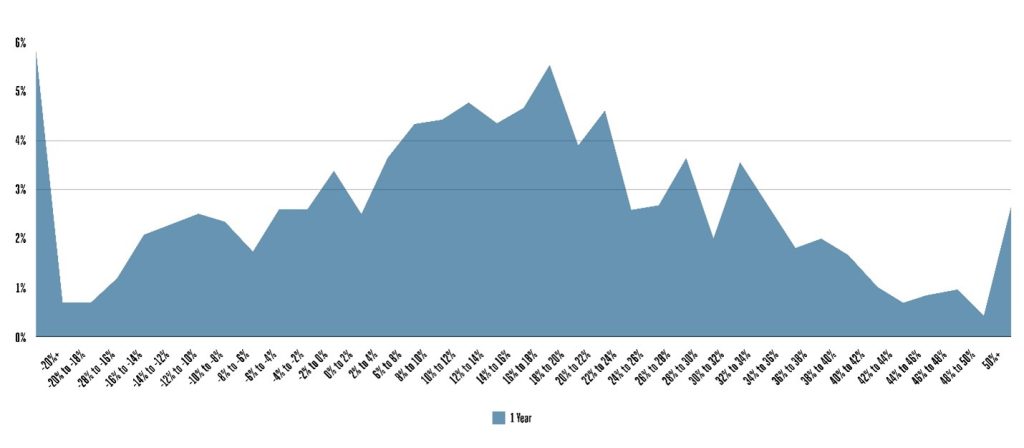

Identical to with the vary of returns, this knowledge is comparatively properly behaved. The longer time intervals have a a lot tighter distribution than the shorter time intervals. In truth, if we focus in on the 1 12 months knowledge – even once we zoom in (check out the variations within the scale), it’s not that a lot a curve.

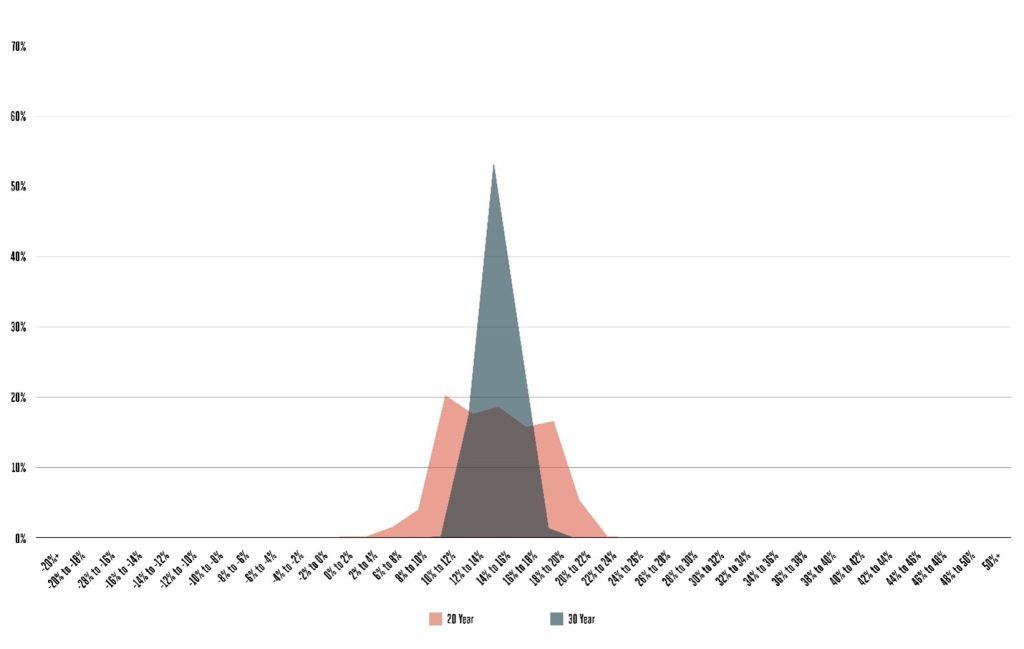

It’s mainly far and wide. There’s just a little little bit of a cluster across the common, however not a lot of 1. Once we examine this to the 20 or 30 12 months observations, we are able to see the distinction very clearly.

With each of those, there’s a really clear curve. They’re largely centered across the common return, however there’s nonetheless just a little little bit of dispersion. With the 20 12 months time intervals, there was just a little bit greater than a 15% likelihood that you’d have an annualized return of lower than 4% and just a little bit greater than a 20% likelihood that your annualized return can be greater than 14%. As a degree of comparability, with the 1 12 months intervals, you’ll have had a 30% likelihood of a return beneath 4% and a virtually 48% likelihood of your return being greater than 14%.

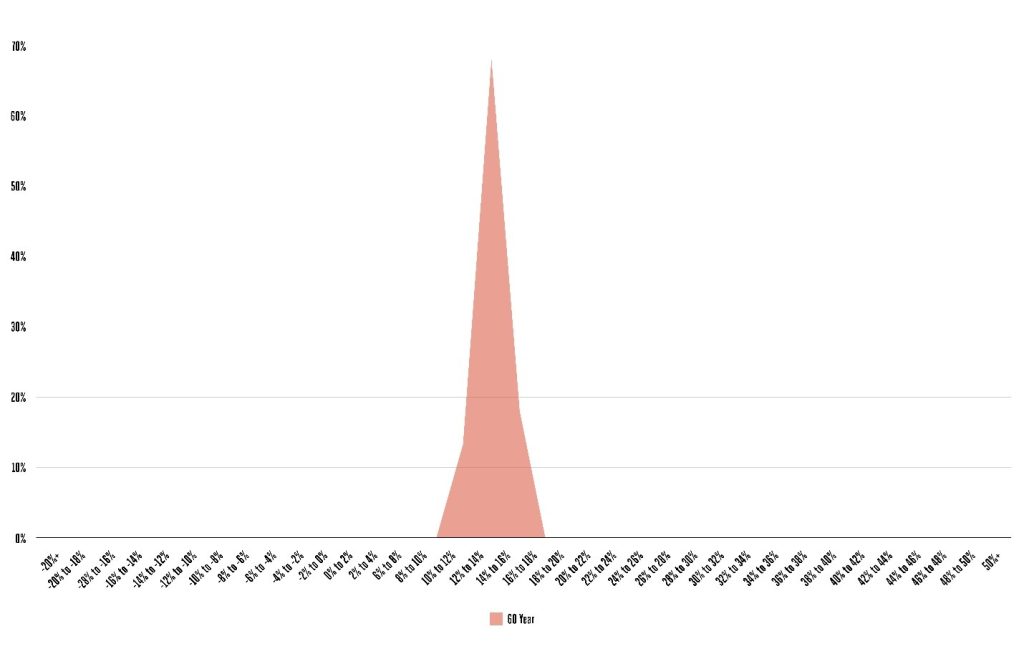

And once we have a look at the 60 12 months interval in isolation, it’s mainly a spike.

There’s technically a distribution right here, however nearly 70% of the observations have been inside a 2 share level vary.

The longer you give your investments to work, the extra assured you could be that you simply’ll have the ability to harvest the chance premia that we talked about – these elementary danger and return relationships out there. There are nonetheless no ensures, however should you wait lengthy sufficient the randomness within the Random Stroll tends to cancel itself out.

However we are able to get much more sensible. Typically, when folks ask what the long run means within the context of investing, they’re asking certainly one of two issues: how lengthy do they have to be invested to be “certain” they don’t lose cash, or that they’ll do higher than some various funding. So let’s have a look at these questions.

We’ll begin with the easier of the 2 – how lengthy you would want to have been invested within the S&P 500 Index to be “certain” that you simply wouldn’t lose cash (we’ll ignore inflation right here for simplicity’s sake). I’ve bought the quotes round certain right here as a result of, once more, there aren’t any ensures in investing. Essentially the most assured that we could be is to say that in the course of the time interval we’re taking a look at there have been no intervals of a selected size the place the S&P 500 misplaced cash. That doesn’t imply it might’t occur sooner or later.

And even ignoring absolute certainty, completely different individuals are comfy with completely different ranges of danger. What it takes for one individual to be “certain” goes to be completely different than what it might take for an additional individual. That is all concerning the various gradations. So in any case that, let’s have a look at the information.

| Holding Interval | % of Observations Larger than 0 |

| 1 Yr | 75.4% |

| 3 Yr | 84.4% |

| 5 Yr | 88.2% |

| 10 Yr | 94.9% |

| 15 Yr | 99.8% |

| 20 Yr | 100.0% |

| 30 Yr | 100.0% |

| 60 Yr | 100.0% |

There are two stuff you in all probability seen instantly:

- The S&P 500 Index does fairly properly should you simply need to keep away from shedding cash (although there are in all probability higher approaches if that is your aim).

- It doesn’t take all that lengthy to be fairly assured (no less than primarily based on this set of knowledge) that you simply received’t lose cash investing within the S&P 500 Index.

The primary level is one everyone knows fairly properly – shares are inclined to go up over time. We wouldn’t be having this dialog if that wasn’t true. And over this time interval (1926 – 2022), the entire annualized return for the S&P 500 Index was 10.12%. However this could really provide you with just a little little bit of pause. Practically 1 / 4 of our 1 12 months intervals had a return greater than 10% lower than the general annualized return for the interval. It’s one factor to take a look at customary deviation numbers, however this helps drive dwelling what that truly means.

The second level is extra particular to our dialog, although. There have been no intervals of 20 years or longer the place the S&P 500 Index misplaced cash. And there have been solely 2 out of 985 15 12 months intervals the place it misplaced cash as properly. Once more, there aren’t any ensures, however this might seemingly make lots of people fairly comfy {that a} 20 12 months holding interval (and even 15 years) can be “long run” sufficient to be fairly assured that may have a constructive return.

However let’s flip to the second (and extra necessary) query. How lengthy do it’s essential make investments to be assured that you simply’ll beat out another funding technique? To maintain issues easy, for our functions that various technique can be proudly owning 5 Yr US Treasury Notes as an alternative of the S&P 500 Index over the identical timeframe. We need to understand how typically we’d have been higher off investing in shares in comparison with bonds (no less than primarily based on the entire returns on the finish of the interval.)

As a degree of comparability, on a month-to-month foundation, over the entire time interval, the S&P 500 beat 5 12 months Treasuries 59% of the time. In different phrases, in 41% of months bonds beat shares.

We all know that shares are inclined to beat bonds over longer time intervals as a result of shares are riskier than bonds, however once more, we’re seeing the Random Stroll in motion. In nearly 5 months of yearly, on common, bonds beat shares.

However what if we have a look at a barely longer time interval than a month?

| Holding Interval | % of Observations Shares Beat Bonds |

| 1 Yr | 66.9% |

| 3 Yr | 72.5% |

| 5 Yr | 74.3% |

| 10 Yr | 82.4% |

| 15 Yr | 86.1% |

| 20 Yr | 98.6% |

| 30 Yr | 100.0% |

| 60 Yr | 100.0% |

We see just about what we anticipated (no less than in a common sense). Shares beat bonds extra typically over a full 12 months than they did every month, however shares nonetheless misplaced a 3rd of the time over the course of a 12 months. In truth, you would want to attend just a little bit longer than 5 years to have a 75% likelihood that the S&P 500 would beat 5 Yr Treasuries. And this isn’t some aggressive benchmark – this is likely one of the foundational relationships in investing. Shares are supposed to beat bonds.

They usually do. You simply want to provide them a while. There have been no 30 or 60 12 months intervals the place shares misplaced to bonds (phew).

There aren’t any clearcut solutions for the way lengthy the “long run” is. However it’s longer than most individuals assume. Investing for the long run doesn’t imply a handful of years. It means many years. It means your investing lifetime. This doesn’t imply that you may’t make modifications alongside the way in which. Your portfolio and retirement plan will change via time. You’ll change via time – your state of affairs in life will change, what you need out of your cash will change. And we’ll discover new methods to take a position that permit us to extra successfully seize the elemental danger and return relationships out there.

However we are able to’t make these modifications as a response to the brief time period, random, gyrations of the market.

As we’ve seen, the Random Stroll actually is random. The market goes to do some simply plain bizarre stuff. We all know this stepping into.

However over time, that randomness (and weirdness) melts away. And what’s left behind are the elemental danger and return relationships within the knowledge – the chance premia that we need to construct our portfolios round.

The trick is that it’s essential decide to your investments. You want to decide to seeing this via to the “long run.” One of many few issues that we are able to say with full confidence is that your investments usually are not going to observe a straight path. They’ll bounce far and wide (keep in mind that chart of the month-to-month S&P 500 returns.) However should you give them the time, their Random Stroll will get you the place you need to go.

{kind=link}